How Much Is a Mortgage on a $500K, $600K, or $700K Home in Northern Virginia?

How Much Is a Mortgage on a $500K, $600K, or $700K Home in Northern Virginia? (2026 Payment Breakdowns)

If you're house hunting in the DMV, the listing price is only the starting point — what really matters is the monthly payment that lands in your bank account every month. With Northern Virginia property taxes, homeowners insurance, and (for many buyers) PMI on top of principal and interest, the difference between a $500,000 home and a $700,000 home can be far more than the $200,000 sticker gap suggests. Below is a complete, line-by-line breakdown of what mortgages on $500K, $600K, and $700K homes actually cost per month in Northern Virginia at today's rates.

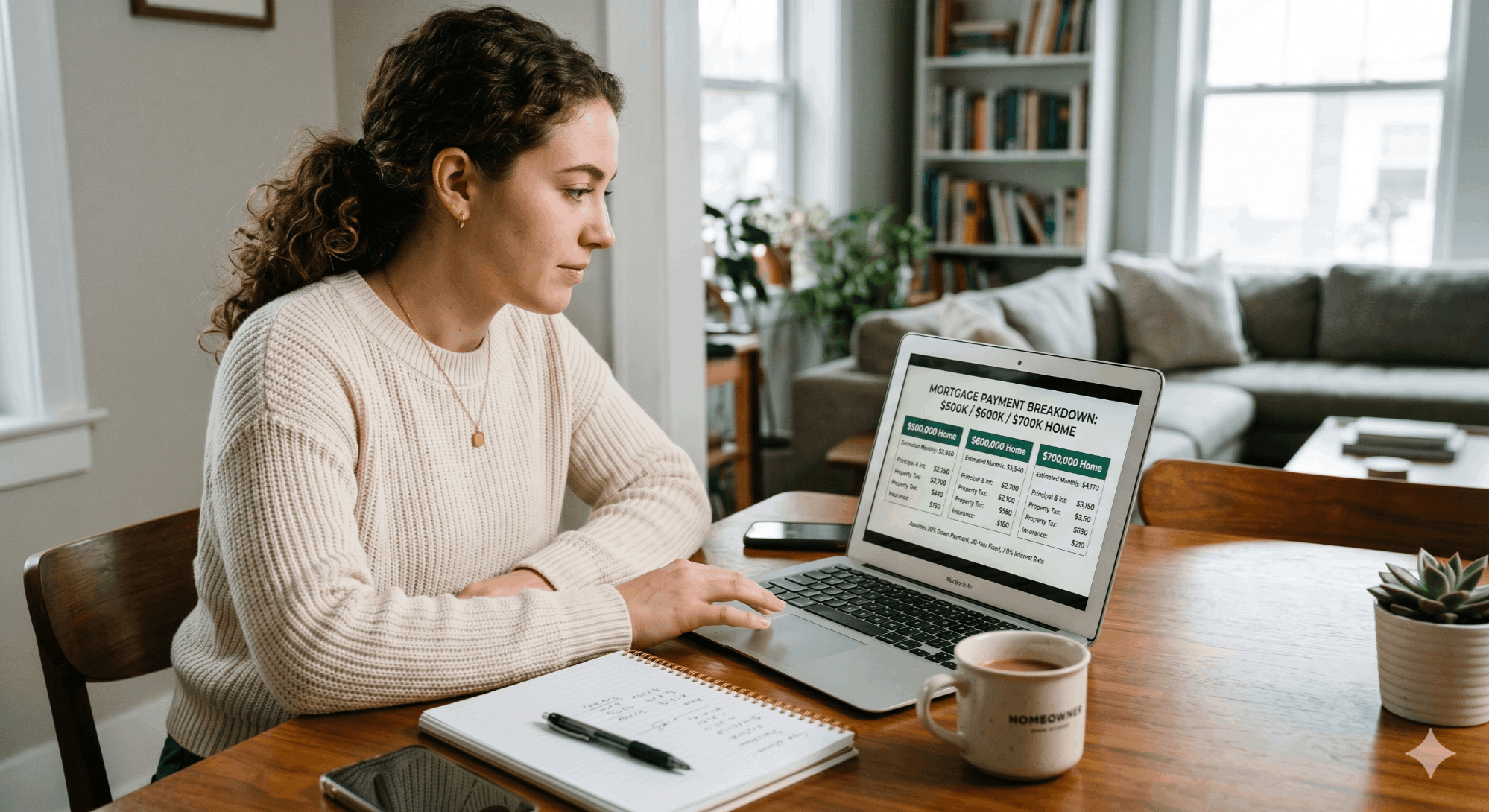

Quick Answer: At today's average 30-year fixed rate of 6.30%, with 10% down and standard Northern Virginia property taxes and insurance, a $500,000 home costs roughly $3,553/month, a $600,000 home runs about $4,259/month, and a $700,000 home comes in near $4,968/month. With 20% down (no PMI), those drop to approximately $3,055, $3,663, and $4,271 per month, respectively. Total payment includes principal, interest, taxes, insurance, and PMI where applicable.

Key Takeaways

- The 30-year fixed rate averaged 6.30% the week of April 16, 2026 — your actual rate will vary based on credit, loan type, and points.

- A "mortgage payment" is really five things: Principal, Interest, Taxes, Insurance — plus PMI if you put down less than 20%, and HOA dues if applicable.

- Northern Virginia property tax rates range from 0.81% in Loudoun County to 1.14% in Alexandria — a $700K home can have a $2,300+ annual tax difference between counties.

- To comfortably afford the monthly payment on a $600K home with 10% down, you typically need a household income around $182,000+ using the 28% housing-to-income rule.

- VA loans (zero down, no PMI) and Virginia Housing down-payment assistance can significantly change your numbers.

In This Guide

- Today's Mortgage Rates and What They Mean

- The Five Components of Your Monthly Payment

- Monthly Payment on a $500,000 Home

- Monthly Payment on a $600,000 Home

- Monthly Payment on a $700,000 Home

- Side-by-Side: $500K vs. $600K vs. $700K

- Property Tax Rates Across Northern Virginia

- How Much Income Do You Need?

- Loan Type Comparison: Conventional, FHA, VA

- Mistakes to Avoid

- Pre-Approval to Closing Timeline

- Frequently Asked Questions

- Glossary

Most online mortgage calculators show a single number — usually principal and interest only — and call it a day. That number is wildly incomplete in Northern Virginia, where property taxes alone can add $400–$650 per month and homeowners insurance another $140–$200. If you're underwriting your own purchase using a stripped-down calculator, you might be planning on a $2,800/month payment when the reality is closer to $3,700.

This guide does the math for you using current rates, real Northern Virginia property tax rates by county, and realistic insurance estimates. Every scenario includes principal, interest, taxes, insurance, and PMI where applicable — the actual number that will hit your bank account each month.

Today's Mortgage Rates and What They Mean for Your Payment

According to Freddie Mac's Primary Mortgage Market Survey released April 16, 2026, the 30-year fixed-rate mortgage averaged 6.30% — a four-week low and roughly half a percentage point below where rates were a year earlier. The 15-year fixed averaged 5.65%. These are national averages for borrowers with strong credit who are putting at least 20% down on a conventional, conforming loan; your individual quote will land slightly above or below depending on your credit profile, loan-to-value ratio, and the points you choose to buy.

| Loan Product | Average Rate (Apr 16, 2026) | One Year Ago | Best For |

|---|---|---|---|

| 30-year fixed | 6.30% | 6.83% | Most buyers wanting predictable, lower payments |

| 15-year fixed | 5.65% | 6.03% | Buyers prioritizing fast equity build, less interest |

A half-point swing in your rate matters more than most buyers realize. On a $500,000 loan, the difference between 6.00% and 6.50% is roughly $160 a month — or nearly $58,000 over the life of a 30-year mortgage. That's why locking your rate at the right moment, and shopping at least three lenders, are two of the highest-leverage decisions you'll make.

ℹ️ All rate-based calculations in this guide use 6.30%

All payment scenarios that follow assume a 30-year fixed loan at 6.30%. If your rate quote comes in higher or lower, your actual payment will scale roughly $30 per month per $500,000 borrowed for every 0.10% change in rate.

The Five Components of Your Monthly Mortgage Payment

When lenders talk about your monthly payment, they're referring to PITI — principal, interest, taxes, and insurance — plus, in many cases, PMI and HOA dues. Each line behaves differently and can be optimized independently:

1. Principal

This is the amount that actually pays down your loan balance. In the early years of a 30-year mortgage, only a small slice of your payment goes to principal — most goes to interest. This flips slowly over time through amortization.

2. Interest

Calculated on your remaining loan balance each month. Because the balance is highest at the start, interest charges are highest at the start — which is why your first few years of payments are largely interest. This is also why refinancing or making extra principal payments early can save tens of thousands in interest.

3. Property Taxes

In Northern Virginia, this is one of the largest non-loan components of your payment. Tax rates vary significantly by county — Loudoun is roughly 0.81%, Fairfax around 1.12%, and Alexandria as high as 1.14%. Your lender will collect 1/12 of your annual tax bill each month and hold it in escrow, then pay the county directly.

4. Homeowners Insurance

Required by every lender. The state average for Virginia hovers around $1,700–$2,200 per year for a typical $300K–$400K dwelling coverage policy, but Northern Virginia homes — which are often newer, larger, and more expensive to rebuild — typically run $1,800–$2,400 annually. Coastal exposure, claims history, and credit also affect the premium.

5. PMI (Private Mortgage Insurance)

If you put down less than 20% on a conventional loan, lenders require PMI to protect them in case of default. PMI typically runs 0.3% to 1.5% of your loan amount annually, with most strong-credit buyers landing near 0.5%. PMI automatically drops off when you reach 22% equity (and you can request removal at 20%). VA loans skip PMI entirely; FHA loans use a similar but separate insurance called MIP that often stays for the life of the loan.

Plus: HOA Dues (Where Applicable)

Townhomes and condos in NOVA almost always have HOA fees ranging from $100 to $400+ per month. Single-family homes in master-planned communities often have a smaller HOA ($30–$100/month). HOA dues are not technically part of your mortgage payment, but they absolutely belong in your monthly housing budget. Skipping them is one of the most common budgeting mistakes new buyers make.

Know your budget, your timeline, and your negotiation position before you step into a single home. Our buyer strategy session is free and covers everything you need to compete in Northern Virginia.

Monthly Payment on a $500,000 Home in Northern Virginia

A $500,000 home today buys you a townhome in many parts of Loudoun and Prince William, a smaller single-family home in outer Fairfax, or a condo in Arlington and Alexandria. Here's what the monthly payment looks like at three common down-payment scenarios, using a 30-year fixed at 6.30%, an estimated NOVA-blended property tax rate of 1.05%, and ~$1,680/year in homeowners insurance.

| Component | 5% Down ($25K) | 10% Down ($50K) | 20% Down ($100K) |

|---|---|---|---|

| Loan Amount | $475,000 | $450,000 | $400,000 |

| Principal & Interest | $2,941 | $2,787 | $2,477 |

| Property Tax | $438 | $438 | $438 |

| Homeowners Insurance | $140 | $140 | $140 |

| PMI (est. 0.5%) | $198 | $188 | $0 |

| Total Monthly Payment | $3,717 | $3,553 | $3,055 |

The $662/month difference between 5% down and 20% down is dramatic — but for many buyers, the larger down payment isn't realistic and the PMI is a fair price for getting into the market years sooner. Run the numbers both ways before deciding.

Monthly Payment on a $600,000 Home in Northern Virginia

$600,000 is a sweet spot in much of NOVA — single-family homes in Centreville, Herndon, and outer Fairfax, larger townhomes in Reston and Ashburn, and quality condos in Tysons and Arlington. Here's the monthly payment math at the same three down-payment scenarios:

| Component | 5% Down ($30K) | 10% Down ($60K) | 20% Down ($120K) |

|---|---|---|---|

| Loan Amount | $570,000 | $540,000 | $480,000 |

| Principal & Interest | $3,530 | $3,344 | $2,973 |

| Property Tax | $525 | $525 | $525 |

| Homeowners Insurance | $165 | $165 | $165 |

| PMI (est. 0.5%) | $238 | $225 | $0 |

| Total Monthly Payment | $4,458 | $4,259 | $3,663 |

If your $600,000 home is in Loudoun County (0.81% tax rate), your property tax line drops from $525 to about $405 — a $120/month savings versus the NOVA average. That's the data-center subsidy at work.

Monthly Payment on a $700,000 Home in Northern Virginia

At $700,000 you're looking at single-family homes in many parts of Fairfax, Reston, Ashburn, and Vienna, larger units in inner-ring locations, or smaller homes in McLean and Great Falls. Here's the math:

| Component | 5% Down ($35K) | 10% Down ($70K) | 20% Down ($140K) |

|---|---|---|---|

| Loan Amount | $665,000 | $630,000 | $560,000 |

| Principal & Interest | $4,118 | $3,902 | $3,468 |

| Property Tax | $613 | $613 | $613 |

| Homeowners Insurance | $190 | $190 | $190 |

| PMI (est. 0.5%) | $277 | $263 | $0 |

| Total Monthly Payment | $5,198 | $4,968 | $4,271 |

The DC-metro 2026 conforming loan limit is $1,249,125, which means a $700K home — even at 5% down — is well within conforming territory and qualifies for the most favorable rates. You don't enter jumbo-loan territory until you cross that threshold.

See exactly what $500K, $600K, or $700K buys today across Fairfax, Loudoun, Prince William, Arlington, and Alexandria. Our search pulls live from the MLS — no stale Zillow data.

Side-by-Side: $500K vs. $600K vs. $700K (10% Down)

Here's the most useful single comparison — the same 10%-down scenario across all three home prices, so you can see exactly how every $100,000 in price translates into your monthly payment:

| Component | $500K Home | $600K Home | $700K Home |

|---|---|---|---|

| Down Payment (10%) | $50,000 | $60,000 | $70,000 |

| Loan Amount | $450,000 | $540,000 | $630,000 |

| Principal & Interest | $2,787 | $3,344 | $3,902 |

| Property Tax | $438 | $525 | $613 |

| Insurance | $140 | $165 | $190 |

| PMI | $188 | $225 | $263 |

| Total Monthly Payment | $3,553 | $4,259 | $4,968 |

| Lifetime Interest (30 yr) | ~$553,300 | ~$663,900 | ~$774,600 |

Each $100,000 step up in home price adds roughly $700 to your monthly payment at 10% down — about $556 in P&I, $87 in property tax, $25 in insurance, and $37 in PMI. That's a useful rule of thumb when you're house hunting and want to translate price differences into payment differences in your head.

Property Tax Rates Across Northern Virginia

In Virginia, property taxes are expressed per $100 of assessed value. The differences between counties may seem small in percentage terms but compound into real money over time.

| Jurisdiction | Real Estate Tax Rate | Annual Tax on $600K Home | Monthly |

|---|---|---|---|

| Loudoun County | $0.805 per $100 (~0.81%) | $4,830 | $403 |

| Prince William County (incl. fire levy) | ~$0.978 per $100 (~0.98%) | $5,868 | $489 |

| Arlington County | $1.013 per $100 (~1.01%) | $6,078 | $507 |

| Fairfax County | $1.1225 per $100 (~1.12%) | $6,735 | $561 |

| Alexandria City | $1.140 per $100 (~1.14%) | $6,840 | $570 |

| Falls Church City | $1.295 per $100 (~1.30%) | $7,770 | $648 |

A $600,000 home in Loudoun versus the same home in Fairfax is a $1,905/year difference in property tax — roughly $159/month. Over a 10-year ownership period, that's nearly $20,000. Loudoun's lower rate is largely subsidized by the data-center concentration in the Ashburn corridor, which generates massive personal-property tax revenue and keeps residential rates lower than neighboring jurisdictions.

⚠️ Don't anchor on the listing's stated tax amount

The "annual taxes" line on a listing usually reflects the previous owner's assessment — which may be years out of date. After your sale closes, the county will reassess at or near your purchase price, and your actual tax bill will go up. Always run your projected payment using the current tax rate against your purchase price, not the listing's historical figure.

How Much Income Do You Need?

The most common rule lenders use is the 28/36 rule: your housing payment should be no more than 28% of your gross monthly income, and total debt payments no more than 36%. Using the conservative 28% threshold for housing alone, here's the household income you'd need for each home price at 10% down:

These are conservative estimates. Many Northern Virginia buyers stretch closer to the 36% threshold, especially if they have minimal other debt. Lenders will often qualify you for higher payments than 28% — but qualifying for a payment and being comfortable with that payment are two different things. Here's what 28% versus 36% looks like in practice:

| Home Price (10% down) | Monthly PITI+PMI | Income at 28% (Conservative) | Income at 36% (Aggressive) |

|---|---|---|---|

| $500,000 | $3,553 | ~$152,300 | ~$118,400 |

| $600,000 | $4,259 | ~$182,500 | ~$141,900 |

| $700,000 | $4,968 | ~$212,900 | ~$165,600 |

Get a clear picture of your purchasing power before you start your search. We'll walk you through pre-approval, budget planning, and what to expect at each price point in NOVA.

Loan Type Comparison: Conventional, FHA, and VA

Loan type can change your monthly payment by hundreds of dollars even at the same purchase price. Northern Virginia is a top destination for military and veteran buyers thanks to the Pentagon, Quantico, Fort Belvoir, and the broader DoD presence — which means VA loans are especially relevant here.

| Loan Type | Min Down | Mortgage Insurance | Best For |

|---|---|---|---|

| Conventional | 3% (5% common) | PMI until 20–22% equity (auto-removable) | Buyers with 700+ credit, can put 5–20% down |

| FHA | 3.5% | MIP for life of loan if <10% down; 11 yr if 10%+ | Buyers with 580–699 credit, lower down payment |

| VA | $0 | None (one-time funding fee, often financed) | Eligible veterans, active duty, surviving spouses |

| USDA | $0 | Annual fee (lower than PMI) | Buyers in eligible rural areas (limited in NOVA) |

For a buyer using a VA loan on a $600,000 home with zero down, the monthly payment would be roughly $4,398 — close to the conventional 5%-down payment of $4,458, but with no down payment required and no PMI. The trade-off is the VA funding fee (typically 2.15% of the loan amount for first-time use, often rolled into the loan), but the cash-flow advantage at closing is enormous.

Mistakes to Avoid When Calculating Your Mortgage

After 840+ closed transactions across the DMV, we see the same handful of budget-busting miscalculations on repeat. Avoid these:

The 7 Biggest Mortgage Math Mistakes

- ✓ Using only "principal & interest" instead of full PITI when budgeting your payment

- ✓ Anchoring on the listing's old tax bill instead of recalculating at your purchase price

- ✓ Forgetting HOA dues — especially on townhomes and condos where they can be $300+/month

- ✓ Assuming PMI is permanent — it auto-drops at 22% equity on conventional loans

- ✓ Using national average insurance rates instead of NOVA-specific quotes

- ✓ Forgetting closing costs (typically 2–3% in Virginia for buyers, on top of down payment)

- ✓ Stretching to 36% DTI without leaving room for furniture, repairs, and emergency reserves

Pre-Approval to Closing — Timeline and Costs

Here's the typical Northern Virginia path from "I'm starting to look" to "I have keys in hand," with the financial milestones at each stage:

Pre-Approval — Week 1

Lender pulls credit, reviews income/assets, issues a written pre-approval letter with a specific loan amount and rate quote. Cost: usually $0 (some lenders charge a small application fee).

House Hunting & Offer — Weeks 2–8

Tour homes, narrow your list, submit an offer. In NOVA's competitive market, expect to write multiple offers before one is accepted. Earnest money deposit (typically 1–3% of purchase price) goes into escrow when your offer is accepted.

Inspection & Appraisal — Weeks 1–2 After Ratified Contract

Home inspection ($400–$700), appraisal ordered by lender ($550–$800), title search initiated. Virginia is a "buyer beware" state — inspections are critical because seller disclosure requirements are limited.

Underwriting & Final Approval — Weeks 2–4

Lender verifies all documentation, issues clear-to-close. Lock your rate if you haven't already. Most NOVA closings happen 30–45 days after a ratified contract.

Closing — Day 30–45

Bring certified funds for down payment and closing costs (typically 2–3% of purchase price in Virginia, including recording fees, title insurance, transfer taxes, and prepaid escrow). Keys handed over the same day in most cases.

Explore Northern Virginia Communities

Fairfax Ashburn Reston Herndon Centreville Vienna Alexandria Prince WilliamKnow your budget, your negotiation position, and exactly what's available — before you tour a single home. The Jamil Brothers provide a full buyer consultation at no cost or obligation.

Frequently Asked Questions

How much is a mortgage on a $500,000 home with 20% down?

At today's 30-year fixed rate of 6.30%, the principal and interest on a $400,000 loan (after $100,000 down) is approximately $2,477 per month. Adding average Northern Virginia property taxes (~$438/month on a $500K home at a 1.05% blended rate) and homeowners insurance (~$140/month) brings the total monthly payment to roughly $3,055. With 20% down, you avoid PMI entirely.

What is the monthly payment on a $700K mortgage at today's interest rate?

A $700,000 home with 10% down ($70K) creates a $630,000 loan. At 6.30% on a 30-year fixed, principal and interest run about $3,902/month. With $613 in average NOVA property taxes, $190 in insurance, and $263 in PMI, the total monthly payment is approximately $4,968. With 20% down (no PMI), it drops to about $4,271.

How much income do I need to afford a $600K house in Northern Virginia?

Using the conservative 28% housing-to-income rule on a $600,000 home with 10% down, you'd need roughly $182,500 in gross household income to comfortably afford the ~$4,259/month payment (PITI plus PMI). At a more aggressive 36% threshold, the income required drops to about $141,900. Lenders will sometimes qualify you above 36% if you have minimal other debt, but staying closer to 28% leaves room for repairs, furniture, and unexpected costs.

What's included in a monthly mortgage payment beyond principal and interest?

Your full monthly payment includes principal, interest, property taxes, and homeowners insurance — collectively known as PITI. If you put down less than 20% on a conventional loan, you'll also pay PMI (private mortgage insurance). FHA loans use a similar charge called MIP. If your home is in an HOA, those dues are a separate but recurring monthly cost. In Northern Virginia, taxes and insurance can easily add $500–$800 per month on top of P&I.

Do I need 20% down to buy a home in Northern Virginia?

No. Conventional loans allow as little as 3% down, FHA loans as little as 3.5%, and VA loans require zero down for eligible borrowers. The trade-off for less than 20% down on a conventional loan is PMI, which typically runs 0.3–1.5% of the loan amount annually. PMI automatically drops off at 22% equity. For most Northern Virginia buyers, putting 5–10% down and paying PMI for a few years is far better than waiting years to save the full 20%.

How does PMI work and when does it go away?

PMI protects the lender if you default. On conventional loans, you pay PMI monthly until you reach 22% equity in the home — at which point it automatically terminates per federal law. You can request manual removal at 20% equity by submitting a written request and (usually) paying for a new appraisal. Note that on FHA loans, the equivalent insurance (MIP) often stays for the life of the loan unless you started with 10%+ down or refinance to a conventional loan.

Why are property taxes so different across Northern Virginia counties?

Each county and city sets its own real estate tax rate annually as part of its budget process. Loudoun County's relatively low rate (~0.81%) is heavily subsidized by personal-property tax revenue from the dense data-center concentration in the Ashburn corridor. Falls Church City has the highest rate in the region (~1.30%) because it's a small jurisdiction with a smaller commercial tax base relative to its services. The difference between Loudoun and Fairfax can mean $1,500–$3,000 per year on a typical $600K home.

Is a 15-year or 30-year mortgage better for Northern Virginia buyers?

It depends on your cash flow and goals. A 15-year fixed at 5.65% (today's average) on a $500,000 loan creates a P&I payment of roughly $4,127/month — versus $3,096/month on a 30-year. The 15-year saves enormous interest over time and builds equity fast, but the higher monthly payment puts more strain on your budget and limits how much house you can qualify for. Most Northern Virginia buyers choose 30-year for the flexibility, then make extra principal payments when they can.

How does a VA loan affect my monthly payment?

VA loans require zero down payment and no monthly mortgage insurance, which significantly reduces the monthly payment compared to a low-down conventional loan. There's a one-time VA funding fee (typically 2.15% of the loan amount for first-time use) that can be financed into the loan. Northern Virginia is a major VA-loan market because of the Pentagon, Quantico, Fort Belvoir, and the broader DoD presence. For eligible veterans and active-duty military, a VA loan is almost always the most powerful financing tool available.

Can I avoid PMI without putting 20% down?

Yes, in a few ways. VA loans never require mortgage insurance. Lender-paid mortgage insurance (LPMI) bakes the cost into your interest rate, eliminating the separate monthly PMI line. Piggyback loans (an 80/10/10 structure) split your financing into a first mortgage of 80%, a second mortgage of 10%, and 10% down — avoiding PMI on the first loan. Each option has trade-offs, and which one is best depends on your loan amount, credit, and how long you plan to own.

How does my credit score affect my mortgage payment?

Credit score is one of the largest single drivers of your interest rate. A buyer with a 760+ score typically gets the lowest available rate; a buyer at 680 may pay 0.25–0.50 percentage points more, which on a $500,000 loan is roughly $80–$160 extra per month. A 620 score will see significantly higher rates and may be limited to FHA financing. If your credit is in the 600s, even a few months of focused improvement before applying can save tens of thousands over the life of the loan.

Should I buy points to lower my mortgage rate in 2026?

Each "point" costs 1% of your loan amount upfront and typically reduces your rate by 0.25%. The math depends on how long you'll keep the loan. On a $500,000 loan, one point costs $5,000 and might save roughly $80/month — meaning a break-even of about 5 years. If you plan to stay in the home 7+ years, points often pencil out. If you might refinance or move within 3–4 years, you'd likely lose money. With rates trending down from a year ago, many buyers are choosing not to pay points and instead planning to refinance later if rates drop further.

Glossary

PITI

Principal, Interest, Taxes, Insurance — the four core components of a monthly mortgage payment.

PMI

Private Mortgage Insurance — required on conventional loans with less than 20% down. Auto-removes at 22% equity.

MIP

Mortgage Insurance Premium — the FHA equivalent of PMI. Often stays for the life of the loan.

Conforming Loan Limit

The maximum loan amount Fannie/Freddie will buy. In the DC metro for 2026, it's $1,249,125.

DTI Ratio

Debt-to-Income — total monthly debt payments divided by gross monthly income. Most lenders cap at 43–50%.

Escrow Account

A holding account your lender uses to collect and pay your property taxes and insurance on your behalf.

Earnest Money Deposit

A good-faith deposit (1–3% of price in NOVA) made when your offer is accepted. Credited at closing.

Discount Points

An upfront fee (1% of loan per point) paid to the lender in exchange for a lower interest rate.

All payment calculations in this guide use the Freddie Mac Primary Mortgage Market Survey rate of 6.30% as of April 16, 2026. Property tax estimates use a Northern Virginia blended rate of 1.05%; actual rates vary by jurisdiction. Insurance estimates use Virginia state averages. Your actual mortgage payment will vary based on credit score, lender, loan type, and the specific home you choose. For a personalized quote, talk to a Jamil Brothers buyer agent or your lender of choice.

Explore More

Browse Every Corner of the DMV Market

Whether you're searching by budget, neighborhood, or buying situation — find exactly what you need below.

Virginia Homes by Budget

Washington DC Homes by Budget

Maryland Homes

Explore Northern Virginia Communities

Loudoun County

Fairfax County & Surrounding

Ready to Make a Move?

Full-Service · No Tradeoffs

List for 1.5% & Keep More Equity

Professional photography, drone video, 3D tours, and expert negotiation — all included. On an $800K home, that's $12,000 more in your pocket vs. a 3% agent.

See the 1.5% Program →Need Speed or Certainty?

Get a No-Obligation Cash Offer

Skip the showings, skip the contingencies. If timing or condition matters more than top dollar, a cash offer may be the right fit. We'll walk you through every option.

Explore Cash Offers →Categories

Recent Posts

Let's Connect