VHDA Loans and Programs: Virginia's Best-Kept Secret for First-Time Buyers (2026)

VHDA Loans and Programs: Virginia's Best-Kept Secret for First-Time Buyers (2026)

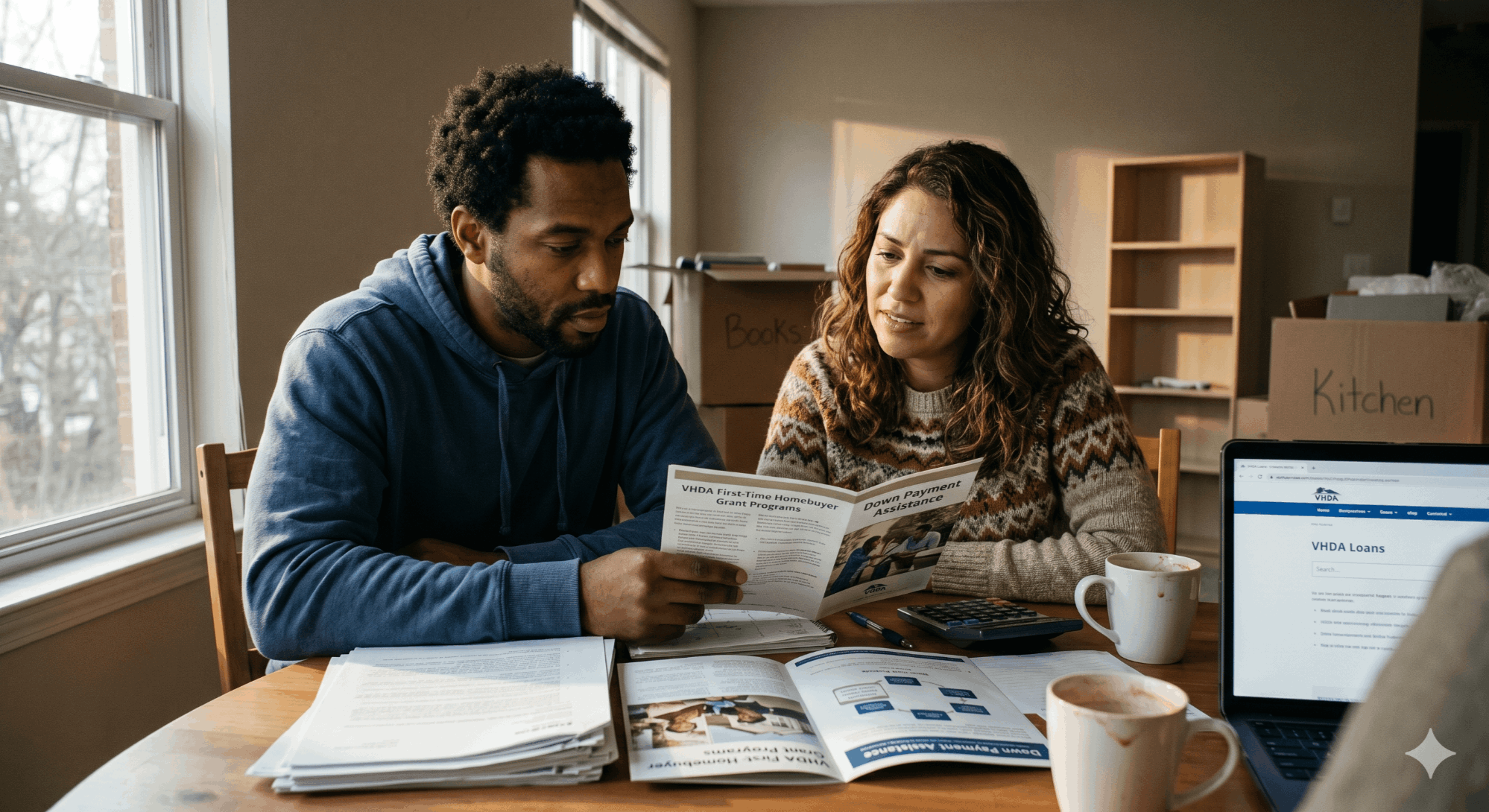

If you're a first-time buyer in Northern Virginia and you've only looked at FHA, conventional, and VA loans, you're missing the most generous state-backed program on the East Coast. Virginia Housing — still widely known by its former name, the Virginia Housing Development Authority, or VHDA — runs a suite of below-market-rate mortgages and non-repayable grants that can cut your out-of-pocket cash at closing by 2% to 5% of the purchase price, and in some cases eliminate the down payment entirely. In Fairfax, Loudoun, Prince William, and Alexandria, that's real five-figure savings.

If you're a first-time buyer in Northern Virginia and you've only looked at FHA, conventional, and VA loans, you're missing the most generous state-backed program on the East Coast. Virginia Housing — still widely known by its former name, the Virginia Housing Development Authority, or VHDA — runs a suite of below-market-rate mortgages and non-repayable grants that can cut your out-of-pocket cash at closing by 2% to 5% of the purchase price, and in some cases eliminate the down payment entirely. In Fairfax, Loudoun, Prince William, and Alexandria, that's real five-figure savings.

Quick Answer: VHDA loans are 30-year fixed-rate mortgages from Virginia Housing (formerly the Virginia Housing Development Authority) that pair competitive interest rates with down payment and closing cost grants. In 2026, qualified first-time buyers in Northern Virginia can receive a non-repayable Down Payment Assistance Grant of 2% to 2.5% of the purchase price, a Closing Cost Assistance Grant of up to 2% on VA and USDA loans, and access to the Plus Second Mortgage for up to 5% of the purchase price — often allowing homeownership with little to no cash at closing. The program's Mortgage Credit Certificate (MCC) has been suspended since May 1, 2023.

Key Takeaways

- VHDA is now Virginia Housing — the agency rebranded in 2021, but the old name stuck with buyers, lenders, and real estate agents across the DMV.

- Five active loan products in 2026: Virginia Housing Conventional, Conventional No MI, FHA, VA, and USDA — all 30-year fixed, all eligible for grant stacking.

- The DPA Grant pays 2% to 2.5% of the purchase price as a true grant — no repayment, no lien, no recapture on refinance or resale.

- Income caps in Northern Virginia reach up to $217,000 for standard programs and $245,000 for expanded/targeted-area programs — far higher than most first-time buyers realize.

- The MCC is gone for now — Virginia Housing suspended the Mortgage Credit Certificate on May 1, 2023. Any article or lender still promoting a new MCC is out of date.

- VHDA programs stack with local Loudoun, Fairfax, Prince William, and Alexandria assistance — creating some of the deepest buyer subsidies available in the DMV.

In This Guide

- What Is a VHDA Loan? (Virginia Housing 101)

- Who Qualifies as a First-Time Buyer in Virginia

- The 2026 VHDA Loan Program Menu

- Virginia Housing Grants and Assistance Programs

- Income and Sales Price Limits in Northern Virginia

- How VHDA Rates Compare to Market Rates in 2026

- MCC Program Status: Suspended Since 2023

- Step-by-Step: Using a VHDA Loan in NOVA

- Local NOVA Programs That Stack with VHDA

- Pros and Cons: Is a VHDA Loan Right for You?

- Common Mistakes Buyers Make with VHDA

- Frequently Asked Questions

- Glossary

Most first-time buyer articles you'll find online treat "VHDA" as a footnote — one bullet in a list of programs, with a single sentence explaining it exists. That's a missed opportunity, because in Northern Virginia, where the median sale price routinely clears $600,000 in Fairfax and Loudoun, a 2% down payment grant is $12,000 to $14,000 you never have to pay back. Add the Plus Second Mortgage for down payment, and you can walk into closing with almost nothing out of pocket on a $500,000 townhome.

This guide walks through every active Virginia Housing program in 2026 — what each one does, who qualifies, how the income and purchase price limits work in Northern Virginia's high-cost counties, and how these programs stack with local Loudoun, Fairfax, Prince William, and Alexandria assistance. We've also flagged what's been quietly suspended (the MCC) and what's been replaced, so you're not planning around a program that no longer exists.

What Is a VHDA Loan? (Virginia Housing 101)

The Virginia Housing Development Authority was created by the Virginia General Assembly in 1972 to make homeownership and affordable rental housing more accessible across the Commonwealth. In 2021, the agency rebranded to "Virginia Housing," but the VHDA name is so entrenched in lender pipelines, MLS listings, and buyer conversations that both names are still used interchangeably. If your Realtor or loan officer says "VHDA," they mean Virginia Housing.

Virginia Housing is self-funded — it raises capital in the bond markets rather than relying on state taxpayer dollars — which is how it can offer below-market rates and non-repayable grants. The agency originates mortgages through approved lender partners (banks, credit unions, and mortgage brokers), and those lenders handle the day-to-day loan process while Virginia Housing sets program rules, caps, and rates.

A "VHDA loan" typically refers to a 30-year fixed-rate mortgage originated under one of Virginia Housing's five active programs, often paired with a Down Payment Assistance Grant, a Closing Cost Assistance Grant, or a Plus Second Mortgage. The defining features are: below-market or market-competitive rates, flexible down payment sources (including grant funds), and required homebuyer education.

ℹ️ Quick Name Reference

VHDA = Virginia Housing Development Authority (legal/historical name). Virginia Housing = current brand name (since 2021). Same agency, same programs, same website at VirginiaHousing.com.

Who Qualifies as a First-Time Buyer in Virginia

The first-time buyer definition used by Virginia Housing is more generous than most buyers expect. You are considered a first-time homebuyer if you have not owned a primary residence in the past three years. That rule — the federal three-year lookback — means that if you owned a home in 2020 but have been renting since 2023, you qualify. Prior ownership in Virginia does not count against you; only ownership in the past three years.

Several groups can qualify even without meeting the three-year rule: single parents who only owned a home with a former spouse, displaced homemakers who only owned with a partner, and veterans purchasing with a VA loan through qualifying Virginia Housing programs. In addition, buyers purchasing in federally designated "Areas of Economic Opportunity" (formerly called targeted areas) can qualify regardless of prior ownership, and those areas often come with higher income and purchase price limits.

Core VHDA Eligibility Checklist

- ✓ Have not owned a primary residence in the past three years (exceptions apply)

- ✓ Minimum credit score of 620 (660 for Conventional No Mortgage Insurance)

- ✓ Debt-to-income ratio of 45% or less (up to 50% allowed in some cases)

- ✓ Complete a Virginia Housing–approved homebuyer education course (free, online or in person)

- ✓ Home must be your primary residence in Virginia

- ✓ Minimum borrower contribution (often 1% of the purchase price) — gift funds allowed

- ✓ Household income and purchase price within program limits for the county

Virginia Housing programs have layered eligibility rules — income, credit, property type, area median limits — that change by county. A 30-minute buyer strategy session tells you exactly which VHDA programs you qualify for and what they'd save you, before you commit to a lender or start touring homes.

The 2026 VHDA Loan Program Menu

Virginia Housing currently offers five active 30-year fixed-rate mortgage programs. All five can be paired with grant programs or the Plus Second Mortgage, and the right choice depends on your credit score, loan type eligibility (military, rural), and whether you want to avoid mortgage insurance.

| Program | Min. Down | Min. Credit | Best For |

|---|---|---|---|

| Virginia Housing Conventional | 3% (1% with DPA) | 640 | Most first-time buyers |

| Conventional No Mortgage Insurance | 3%+ | 660 | Buyers with strong credit avoiding PMI |

| Virginia Housing FHA | 3.5% | 620 | Lower credit scores, smaller down payment |

| Virginia Housing VA | 0% | 620 | Eligible veterans, active duty, surviving spouses |

| Virginia Housing USDA/RHS | 0% | 620 | Rural properties (limited NOVA options) |

Virginia Housing Conventional: The Workhorse

The Virginia Housing Conventional is the most commonly used VHDA product. It's a standard 97%-LTV conventional mortgage (so 3% down) that requires private mortgage insurance while your loan-to-value is above 80%. The 640 credit score minimum is typical, and sellers can contribute up to 3% toward closing costs. What makes it different from a standard Fannie Mae Conventional 97 is program stacking — you can combine it with the DPA Grant and Plus Second Mortgage, and pay as little as 1% of the purchase price out of pocket.

Conventional No Mortgage Insurance: The PMI Killer

This program is nearly identical to the standard Conventional, with one major difference: no private mortgage insurance, even below 20% down. The trade-off is a higher credit score requirement (660 minimum) and a slightly higher interest rate that builds the insurance cost into the rate itself. For buyers with strong credit who plan to stay in the home for 5 to 7+ years, this program often beats the standard Conventional on lifetime cost.

Virginia Housing FHA

The FHA option is Virginia Housing's answer for buyers with lower credit (620+) or higher debt-to-income ratios. It carries standard FHA mortgage insurance (an upfront premium of 1.75% and annual MIP), which sticks for the life of the loan on most FHA loans originated since 2013. The 2026 FHA loan limit for Northern Virginia high-cost counties — Arlington, Fairfax, Loudoun, Prince William, Alexandria, Falls Church, Manassas, and Manassas Park — is $1,209,750.

Virginia Housing VA Loan

For eligible veterans, active duty service members, and some surviving spouses, the Virginia Housing VA loan combines zero-down VA financing with Virginia Housing's Closing Cost Assistance Grant (up to 2% of the purchase price). The VA funding fee can be paid with grant funds, which means military buyers in Northern Virginia — a population concentrated around the Pentagon, Quantico, Fort Belvoir, and Joint Base Myer-Henderson Hall — can often close with only inspection and appraisal costs out of pocket.

Virginia Housing Grants and Assistance Programs

This is where VHDA earns its "best-kept secret" reputation. The grants and second mortgages attached to the loan programs above are what make Virginia Housing genuinely different from a standard Fannie Mae or FHA loan.

Down Payment Assistance (DPA) Grant

The DPA Grant provides 2% to 2.5% of the home's purchase price as a true grant — it never has to be paid back, even if you sell or refinance. It can be paired with the Virginia Housing Conventional, Conventional No MI, or FHA loan, and requires a minimum 620 credit score. On a $500,000 NOVA townhome, that's $10,000 to $12,500 in non-repayable help.

Closing Cost Assistance (CCA) Grant

The CCA Grant provides up to 2% of the purchase price — but it's only available on Virginia Housing VA and USDA first mortgages. Funds can be applied to closing costs, discount points, prepaid items, the VA funding fee, or the USDA guarantee fee. Like the DPA Grant, it's non-repayable and requires no lien on the property.

Plus Second Mortgage

The Plus Second Mortgage is a second-position loan for 3% to 5% of the purchase price, used for down payment and — for buyers with 680+ credit — closing costs. Unlike the DPA Grant, this is a loan that must be repaid, typically amortized over 30 years at a fixed rate. The advantage: it stacks with a first mortgage for a combined loan-to-value of up to 100% or slightly above, meaning you can potentially buy with zero down even on a conventional loan.

SPARC Program (Sponsoring Partnerships and Revitalizing Communities)

SPARC isn't a grant or a loan — it's an interest rate discount. Virginia Housing allocates pools of funding to participating local governments and nonprofits, who in turn offer a 1% rate reduction on qualifying VHDA mortgages for their first-time buyers. Both Loudoun County and the City of Alexandria participate. The catch: SPARC is an allocation, not a guarantee — once the local pool runs out, the 1% reduction disappears until the next funding cycle.

Granting Freedom (Disabled Veterans)

Granting Freedom is a Virginia Housing partnership with the Virginia Department of Veterans Services, providing up to $8,000 in grant funds for home modifications for veterans and service members who sustained a line-of-duty injury resulting in a service-connected disability. Funds can cover ramps, widened doorways, grab bars, roll-in showers, and other accessibility modifications. It applies to both owned homes and rental units.

| Program | Amount | Repayment | Paired With |

|---|---|---|---|

| DPA Grant | 2% – 2.5% of price | None (grant) | VA Housing Conv, No MI, FHA |

| CCA Grant | Up to 2% of price | None (grant) | VA Housing VA, USDA |

| Plus Second Mortgage | 3% – 5% of price | Yes (second lien) | Any VHDA first mortgage |

| SPARC Rate Reduction | 1% lower interest rate | None (allocation) | Any VHDA first mortgage |

| Granting Freedom | Up to $8,000 | None (grant) | Home modifications (any loan) |

Income and Sales Price Limits in Northern Virginia

Virginia Housing sets income and sales price / loan limits that vary by the metropolitan area, and they're meaningfully higher in Northern Virginia than anywhere else in the state. The baseline limits — for Richmond, Virginia Beach, and most smaller markets — are substantially lower than what applies in Fairfax, Loudoun, Prince William, Arlington, and Alexandria.

For Northern Virginia high-cost jurisdictions in 2026, standard program maximum household incomes sit between roughly $148,000 and $174,000, depending on household size. Expanded programs — which apply in designated Areas of Economic Opportunity and for some buyer types — extend income eligibility up to approximately $245,000 for NOVA, with a maximum loan amount of $806,500 statewide and $800,000 on most lender-marketed VHDA programs for the region.

⚠️ Limits Change Annually

Virginia Housing updates income and sales price limits each year (usually mid-year, effective for new applications locked after the update date). Always verify the current limits with a Virginia Housing–approved lender for the specific county where you're buying before you write an offer.

What This Looks Like in Practice

On a $525,000 townhome in Ashburn with the Virginia Housing Conventional plus a 2.5% DPA Grant, a qualifying buyer with a 720 credit score and $125,000 household income would see grant funds of $13,125 applied toward the down payment — leaving just 0.5% ($2,625) plus closing costs to cover out of pocket. On a $575,000 townhome in Arlington with the Conventional No MI program, the same buyer avoids PMI entirely, which saves roughly $150 to $200 a month on a $557,000 loan. Those are real dollars that compound over the life of the mortgage.

Virginia Housing's purchase price limits and loan caps mean you'll want to filter your home search carefully. Our live MLS-powered search at thejamilbrothers.com/homes-for-sale lets you filter by price, county, school district, and property type — and it pulls directly from BrightMLS with no stale Zillow data.

How VHDA Rates Compare to Market Rates in 2026

Virginia Housing publishes daily rates that typically sit at or slightly below market averages. As of mid-April 2026, the average 30-year fixed mortgage rate in Virginia is around 6.30%, while the 15-year fixed sits near 5.88%. VA loan rates, both standalone and through Virginia Housing, run meaningfully lower — often in the mid-5% range.

Where VHDA rates genuinely outperform is on the Conventional No Mortgage Insurance program and on any program paired with SPARC. A 1% SPARC rate reduction on a $500,000 loan saves roughly $315 per month on principal and interest at current rates. Over a 30-year term, that's over $113,000 in interest savings — assuming you stay in the home and don't refinance.

Rate Comparison: $500K Loan, 30-Year Fixed (Illustrative)

Rates illustrative and change daily. Virginia Housing publishes current rates at VirginiaHousing.com. Actual rate depends on credit, loan type, and lender.

MCC Program Status: Suspended Since 2023

⚠️ The MCC Is No Longer Available to New Borrowers

Virginia Housing's Mortgage Credit Certificate (MCC) program is suspended as of May 1, 2023. Loans locked after April 28, 2023 are not eligible for an MCC. If a lender, article, or older buyer guide mentions the VHDA MCC as an active benefit, it is outdated.

Before the suspension, the MCC was a federal tax credit worth up to 10% of annual mortgage interest, claimed every year for the life of the loan as long as the homeowner lived in the property. For many NOVA buyers, it was worth $1,500 to $2,000 per year in reduced federal income taxes. Its suspension removed one of the most financially significant pieces of the VHDA toolkit.

Good news for existing MCC holders: if you received an MCC on or before April 28, 2023, you keep it for the life of that mortgage, as long as you continue to live in the home. Refinancing the mortgage, however, cancels the MCC. Virginia Housing has not announced a firm restart date for the program, and any restart would require new bond allocations — so don't plan your 2026 or 2027 purchase around it.

Step-by-Step: Using a VHDA Loan in Northern Virginia

Book a Buyer Strategy Session — Week 1

Before you talk to a single lender, sit down with a buyer's agent who knows the VHDA product suite cold. A strategy session covers which VHDA program fits your credit, income, and target price, and whether local NOVA programs can stack on top.

Choose a Virginia Housing–Approved Lender — Week 2

Not every lender is approved to originate VHDA loans. Virginia Housing maintains a list of approved lenders, and your buyer's agent can recommend ones with strong VHDA experience. Getting pre-approved specifically under a VHDA program takes 3 to 5 business days.

Complete Homebuyer Education — Weeks 2–3

Virginia Housing requires all VHDA borrowers to complete a homebuyer education course. Free online courses take 6 to 8 hours and can be done before or during your home search. Get your completion certificate and store it — your lender will need it before closing.

Tour Homes and Write Offers — Weeks 3–8

Write offers with your VHDA pre-approval letter attached. In Northern Virginia's competitive market, listing agents will scrutinize your financing — your agent can help position VHDA as a strength (government-backed program, firm pre-approval) rather than a perceived weakness.

Lock Your Rate and Grants — At Contract Ratification

Once you're under contract, your lender submits the file to Virginia Housing for program approval and rate lock. DPA Grant, CCA Grant, or SPARC allocations are reserved at this point. SPARC in particular is first-come, first-served within the annual county allocation.

Underwriting and Closing — 30 to 45 Days

VHDA underwriting runs through Virginia Housing after your lender's initial underwriting. Expect a 30- to 45-day close from contract ratification. Grant funds are applied at closing, not disbursed to you — so they reduce cash-to-close rather than showing up in your account.

Local NOVA Programs That Stack with VHDA

Several Northern Virginia jurisdictions run their own first-time buyer assistance programs, and most are designed to layer on top of a VHDA first mortgage. Combining them can push total assistance into the $40,000 to $80,000 range on a single transaction.

Loudoun County: DPCC, DPCC Plus, PEG, and SPARC

Loudoun County's Down Payment/Closing Cost Assistance (DPCC) program offers up to 10% of the sales price or $70,000, whichever is less, forgivable over a 15-year period with no interest. Applicants must live or work in Loudoun County for at least six months, and gross annual household income must fall within 30% to 70% of the Area Median Income — a current eligible range of $49,200 to $114,749 regardless of family size. The DPCC Plus program extends eligibility to 70% to 100% of AMI (roughly $114,750 to $163,900). Loudoun County also runs a Public Employee Homeownership Grant (PEG) of $25,000 for full- or part-time employees of the county government, courts, constitutional officers, and Loudoun County Public Schools.

Loudoun's SPARC allocation for FY2025 was $8 million — the largest in the state — though as of August 15, 2025, funding for FY2026 was not yet available, with updates posted when the new allocation comes through. Buyers should check with a Virginia Housing–approved lender before writing an offer to see whether current-year funds are still available.

Alexandria: Flexible Homeownership Assistance Program + SPARC

The City of Alexandria's Flexible Homeownership Assistance Program offers eligible first-time buyers a shared-equity loan of up to $50,000 (for buyers under 100% AMI) or $75,000 (for buyers under 80% AMI), plus a 1% SPARC rate reduction through Virginia Housing. The city also runs a Neighborhood Stabilization Program in partnership with Rebuilding Together Alexandria, acquiring and renovating distressed properties for sale to income-eligible first-time buyers who live or work in the city.

Fairfax County: First-Time Homebuyers Program

Fairfax County offers below-market-price homes to first-time buyers through its First-Time Homebuyers Program, which requires a Virginia Housing homebuyer education course and a lender pre-approval. Homes are allocated via drawings, and income/residency requirements apply. It's one of the most competitive first-time buyer paths in the region — applications often run 10 to 30 deep per available home.

Prince William County: DPA Program

Prince William County, along with the cities of Manassas and Manassas Park, offers a Down Payment Assistance program providing up to 6% of the purchase price for low- to moderate-income buyers (at or below 80% AMI). This is particularly valuable given Prince William's lower median price — roughly $150,000 to $200,000 below Fairfax — which keeps buyers comfortably within VHDA purchase price limits.

VHDA, SPARC, DPCC, Flexible Homeownership, PEG — these programs change yearly, and stacking them requires coordination between your agent, lender, and county housing office. With 840+ homes sold across the DMV, we know which lenders actually close VHDA deals and which local programs are currently funded.

Pros and Cons: Is a VHDA Loan Right for You?

| ✓ Pros | ✗ Cons |

|---|---|

| Non-repayable DPA Grant of 2% – 2.5% | Income and purchase price limits apply |

| Stacks with local Loudoun, Fairfax, PWC, Alexandria programs | Slightly slower underwriting (adds ~5 days to close) |

| Competitive or below-market rates | Must use a Virginia Housing–approved lender |

| Conventional No MI option skips PMI entirely | Max loan amount $806,500 (below NOVA jumbo threshold) |

| SPARC 1% rate reduction where available | MCC suspended — tax credit no longer available |

| Homebuyer education is free and permanent benefit | Recapture tax possible on bond-funded loans sold in < 9 years |

Common Mistakes Buyers Make with VHDA

After watching hundreds of first-time buyers work through Virginia Housing programs, the same avoidable mistakes keep showing up. Here are the patterns worth knowing before you file an application.

Avoid These VHDA Pitfalls

- ✗ Planning around the MCC. It's been suspended since May 2023. Budget without it.

- ✗ Using a non-approved lender. Many NOVA mortgage brokers don't originate VHDA loans — confirm before pre-approval.

- ✗ Waiting to take homebuyer education. File your certificate early — it's free and required.

- ✗ Assuming SPARC is always available. County allocations run out — confirm funding before writing an offer.

- ✗ Ignoring the DTI cap. VHDA maxes out at 45% – 50% DTI; a strong pre-approval requires careful debt management.

- ✗ Forgetting the recapture tax. Homes financed with tax-exempt bond funds may trigger a federal recapture tax if sold within 9 years.

Frequently Asked Questions

What is a VHDA loan in 2026?

A VHDA loan is a 30-year fixed-rate mortgage originated through Virginia Housing (formerly the Virginia Housing Development Authority, or VHDA) under one of its five active programs: Virginia Housing Conventional, Conventional No Mortgage Insurance, FHA, VA, and USDA. VHDA loans are typically paired with a non-repayable Down Payment Assistance Grant of 2% to 2.5% of the purchase price, a Closing Cost Assistance Grant of up to 2% (on VA and USDA loans), or a Plus Second Mortgage of 3% to 5% of the purchase price. The agency rebranded to Virginia Housing in 2021, but the VHDA name is still widely used.

How much is the VHDA DPA Grant worth?

The Virginia Housing Down Payment Assistance Grant is worth 2% to 2.5% of the home's purchase price, depending on the first mortgage type. It is a true grant — no repayment, no lien, no recapture on refinance or resale. On a $500,000 Northern Virginia home, that translates to $10,000 to $12,500 in non-repayable help applied at closing. To qualify, buyers need a minimum 620 credit score, must meet income and purchase price limits for the county, and must use a VHDA Conventional, Conventional No MI, or FHA first mortgage.

Is the VHDA MCC program still active in 2026?

No. The Virginia Housing Mortgage Credit Certificate (MCC) program has been suspended since May 1, 2023. Loans locked after April 28, 2023 are not eligible for an MCC. Homeowners who received an MCC on or before that date keep the benefit for the life of their mortgage, as long as they continue to live in the home — but new buyers cannot receive one. Any current lender or blog promoting a new VHDA MCC is working from outdated information.

Can I use a VHDA loan in Fairfax County or Loudoun County?

Yes. VHDA loans are available statewide, including in all Northern Virginia high-cost jurisdictions — Fairfax County, Loudoun County, Prince William County, Arlington County, the City of Alexandria, and the independent cities of Falls Church, Fairfax, Manassas, and Manassas Park. The income and purchase price limits in these counties are substantially higher than the state baseline to reflect the high-cost DMV housing market. Buyers in these areas also get access to local stacking programs like Loudoun's DPCC, Fairfax County's First-Time Homebuyers Program, Alexandria's Flexible Homeownership Assistance, and Prince William's 6% DPA program.

What are the VHDA income limits for Northern Virginia in 2026?

Income limits vary by program and change annually. For standard VHDA programs in Northern Virginia high-cost jurisdictions, maximum household income typically falls between $148,000 and $174,000. Expanded programs — which apply in designated Areas of Economic Opportunity — extend income eligibility up to approximately $245,000 in NOVA. Maximum loan amount is $806,500 statewide (most lender-marketed VHDA programs in NOVA cap at $800,000). Always verify current limits with a Virginia Housing–approved lender for the specific county where you're buying.

What credit score do I need for a VHDA loan?

The minimum credit score depends on the program: 620 for Virginia Housing FHA, VA, and USDA loans, 640 for the Virginia Housing Conventional, and 660 for the Conventional No Mortgage Insurance program. The Plus Second Mortgage requires 680+ to use funds for closing costs (the down payment use has a lower bar). Credit score affects both eligibility and the interest rate you'll receive — stronger credit usually earns a lower published VHDA rate.

Are VHDA interest rates actually lower than market rates?

VHDA rates are typically at or slightly below market — the largest rate advantage comes from the SPARC program, which subtracts 1% from the VHDA rate for buyers in participating jurisdictions like Loudoun County and the City of Alexandria. The Conventional No Mortgage Insurance program also provides a meaningful monthly savings by eliminating PMI, even though its headline rate is slightly higher. For buyers comparing apples to apples, the total cost of borrowing (rate + PMI + fees) is usually lower with VHDA than with a standard conventional or FHA loan.

Do I need a buyer's agent to use a VHDA loan?

You're not required to have a buyer's agent, but after the August 2024 NAR settlement changes, working without one in Northern Virginia is risky. VHDA loans add an extra layer of complexity — program selection, grant stacking, SPARC timing, local program eligibility — and a strong buyer's agent coordinates that across the lender, listing agent, and settlement company. Buyers now sign written buyer-broker representation agreements before touring homes. The Jamil Brothers Realty Group offers a free buyer strategy session at thejamilbrothers.com/buyer-strategy that covers VHDA program selection before you sign any agreement.

Can I combine VHDA with local Loudoun, Fairfax, or Alexandria programs?

Yes, and this is where the largest buyer savings come from. Most local NOVA programs — Loudoun County DPCC and PEG, Alexandria's Flexible Homeownership Assistance, Fairfax County's First-Time Homebuyers Program, and Prince William's DPA — are designed to stack on top of a VHDA first mortgage. Combined with a VHDA DPA Grant and SPARC, total assistance on a single transaction can reach $40,000 to $80,000. Coordination matters, though — the lender, county housing office, and Virginia Housing all have to approve the stacking, which takes additional time during underwriting.

Is now a good time to use a VHDA loan in Northern Virginia?

For buyers who qualify, yes. Northern Virginia inventory has loosened modestly in 2026 compared to the 2021–2022 crunch, but NOVA median prices remain in the $600,000+ range in Fairfax and Loudoun. With standard 30-year fixed rates around 6.30% and VA rates in the mid-5% range, VHDA's DPA Grant and SPARC rate reduction are more valuable than they were during the low-rate years. The grants reduce upfront cash needed; SPARC reduces monthly payment. Both are durable benefits regardless of where rates go next.

What is the VHDA recapture tax, and when does it apply?

The federal recapture tax is a one-time tax that may apply if three conditions are met: your VHDA loan was financed with tax-exempt bond funds (or you had an MCC), you sell your home within nine years of purchase, and your income at sale exceeds allowable federal limits. Most buyers never owe any recapture tax because they either stay past nine years, their income doesn't rise enough, or home appreciation falls within the allowable band. Virginia Housing offers a recapture tax calculator on its website, and the agency actually reimburses the tax for many eligible borrowers.

How long does a VHDA loan take to close?

Expect 30 to 45 days from contract ratification to closing — about five days longer than a non-VHDA conventional loan because of the second layer of underwriting (your lender first, then Virginia Housing). Experienced VHDA lenders close consistently inside 35 days; inexperienced lenders often stretch to 45 or beyond. Starting homebuyer education early (before you're under contract) and providing complete income documentation upfront are the two biggest accelerators.

Glossary

VHDA / Virginia Housing

Self-supporting Virginia state housing agency (1972 founding, rebranded 2021) that originates first-time buyer mortgages through approved lenders.

DPA Grant

Down Payment Assistance Grant. Virginia Housing's flagship grant worth 2% to 2.5% of purchase price; fully non-repayable.

CCA Grant

Closing Cost Assistance Grant. Up to 2% of purchase price; available only on VHDA VA and USDA first mortgages.

Plus Second Mortgage

A repayable second lien from Virginia Housing worth 3% to 5% of purchase price, used for down payment (and closing costs with 680+ credit).

SPARC

Sponsoring Partnerships and Revitalizing Communities. Local-government-allocated 1% rate reduction on VHDA mortgages.

MCC

Mortgage Credit Certificate. Federal tax credit worth up to 10% of annual mortgage interest. Suspended by Virginia Housing since May 1, 2023.

Area of Economic Opportunity

Federally designated census tracts where higher income and purchase price limits apply; first-time buyer rule is often waived.

Recapture Tax

A one-time federal tax potentially owed if you sell a bond-funded VHDA home within 9 years at higher income; often reimbursed by Virginia Housing.

Conclusion and Next Steps

Virginia Housing programs are the single most underused lever first-time buyers have in Northern Virginia. The DPA Grant alone is worth more than a year of aggressive saving for most NOVA households. Stack it with SPARC, a local county program, and the Plus Second Mortgage, and the total subsidy can exceed $50,000 on a single $500,000 purchase — all while getting a rate that's at or below what you'd get from a standard bank.

The catch is that VHDA isn't plug-and-play. Programs change yearly. Income and purchase price limits move. SPARC allocations empty. The MCC is gone. Local stacking requires coordination between your Realtor, lender, and county housing office, and not every NOVA lender is VHDA-approved. That's why most buyers either miss these programs entirely or leave money on the table even when they use one.

The Jamil Brothers Realty Group has helped over 840 buyers and sellers across the DMV navigate exactly this complexity. If you're thinking about buying in the next 6 to 12 months, start with a free buyer strategy session — no pressure, no obligation, just a clear picture of which VHDA programs you qualify for and how to use them to buy the right home.

Know exactly which VHDA programs you qualify for, how they stack with local NOVA assistance, and what it all means for your cash-to-close — before you shop a single listing. Our strategy sessions are free, no-obligation, and tailored to your price range and target neighborhoods.

Explore Northern Virginia Communities

Fairfax Ashburn Leesburg Reston Herndon Centreville Alexandria Prince WilliamAlready know what you want to see? Browse every active listing in Northern Virginia — updated live from BrightMLS — at thejamilbrothers.com/homes-for-sale, or request a free home evaluation if you're selling first to fund your purchase.

Explore More

Browse Every Corner of the DMV Market

Whether you're searching by budget, neighborhood, or buying situation — find exactly what you need below.

Virginia Homes by Budget

Washington DC Homes by Budget

Maryland Homes

Explore Northern Virginia Communities

Loudoun County

Fairfax County & Surrounding

Ready to Make a Move?

Full-Service · No Tradeoffs

List for 1.5% & Keep More Equity

Professional photography, drone video, 3D tours, and expert negotiation — all included. On an $800K home, that's $12,000 more in your pocket vs. a 3% agent.

See the 1.5% Program →Need Speed or Certainty?

Get a No-Obligation Cash Offer

Skip the showings, skip the contingencies. If timing or condition matters more than top dollar, a cash offer may be the right fit. We'll walk you through every option.

Explore Cash Offers →Categories

Recent Posts

Let's Connect