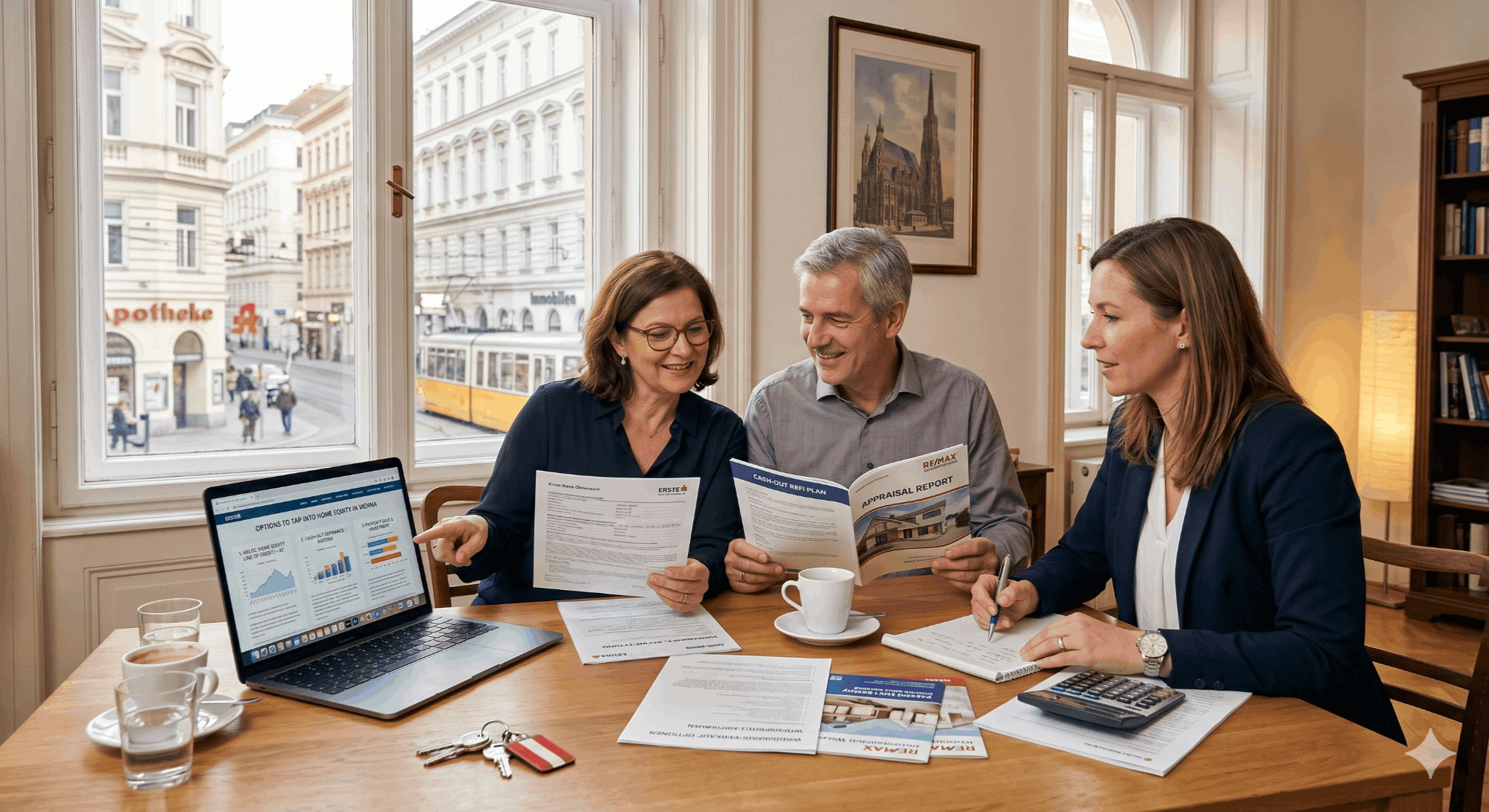

Tapping Into Home Equity in Vienna: HELOC, Cash-Out Refi & Sale Options

Tapping Into Home Equity in Vienna: HELOC, Cash-Out Refi & Sale Options

Vienna, VA · Fairfax County · Updated for 2026 market conditions

Quick Answer: Vienna homeowners have three primary ways to access home equity: a HELOC (line of credit secured by the home, typically prime + 0.5% to prime + 2%), a cash-out refinance (replaces your existing mortgage with a larger one), or selling the home outright. With Vienna median values around $1.1M+ and many long-term owners sitting on $400K–$800K+ in equity, the right choice depends on your interest-rate position, how much cash you need, and whether you plan to stay or relocate.

Key Takeaways

- Vienna equity is unusually strong — homes in 22180/22181/22182 have appreciated significantly since 2018, and many long-term owners have $500K+ in tappable equity.

- HELOCs preserve your low-rate first mortgage — ideal if you locked a sub-4% rate in 2020–2021 and only need partial liquidity.

- Cash-out refinances make sense when current rates are at or below your existing rate — otherwise you trade a low payment for a higher one.

- Selling unlocks 100% of your equity in one transaction — and with The Jamil Brothers' 1.5% full-service listing program, Vienna sellers keep meaningfully more of that equity at closing.

- Tax treatment differs sharply — interest deductibility, capital gains, and the $250K/$500K primary-residence exclusion all change the math.

- Run the numbers before you decide — a free Vienna home valuation and a personalized net sheet make the comparison concrete instead of theoretical.

In This Guide

- How Much Equity Vienna Homeowners Have in 2026

- The Three Primary Ways to Access Equity

- Option 1 — HELOC: How It Works in Vienna

- Option 2 — Cash-Out Refinance: When the Math Works

- Option 3 — Selling Your Vienna Home

- Side-by-Side Comparison: HELOC vs. Refi vs. Sale

- Vienna Sale Net Proceeds Calculator

- Tax Implications You Need to Understand

- Five Common Scenarios — Which Option Fits

- Mistakes to Avoid When Tapping Equity

- How to Choose the Right Path

- Frequently Asked Questions

- Glossary

Vienna sits in one of the most equity-rich pockets of Northern Virginia. Walkable downtown Maple Avenue, Vienna Metro, and the school catchments for Madison, Marshall, and Oakton High Schools have produced years of compounding appreciation — and many homeowners now find themselves sitting on hundreds of thousands of dollars in unrealized gains. The question for 2026 is not whether you have equity. It is how to access it without giving more of it away than necessary.

This guide walks through the three real options Vienna homeowners actually have — a Home Equity Line of Credit, a cash-out refinance, and an outright sale — and compares them side by side using realistic Vienna numbers. The right answer depends on your current mortgage rate, how much liquidity you need, your tax situation, and whether your long-term plan involves staying in Vienna or moving on.

How Much Equity Vienna Homeowners Have in 2026

Equity is the difference between what your home is worth today and what you still owe on it. In Vienna, that gap has widened considerably for most owners who purchased before the 2022 rate cycle. Median home values in the 22180, 22181, and 22182 ZIP codes have moved into the low $1.1M–$1.4M range depending on neighborhood, lot size, and renovation status — well above where many of today's homeowners purchased.

Equity gains by purchase year — typical Vienna single-family

| Purchased | Typical Purchase Price | Approx. 2026 Value | Estimated Equity Range* |

|---|---|---|---|

| 2014–2016 | $650K–$800K | $1.2M–$1.5M | $500K–$800K+ |

| 2017–2019 | $750K–$950K | $1.2M–$1.5M | $400K–$700K |

| 2020–2021 | $900K–$1.1M | $1.2M–$1.5M | $250K–$500K |

| 2022–2024 | $1.05M–$1.3M | $1.2M–$1.5M | $100K–$300K |

*Equity range assumes 20% down at purchase, standard amortization, no second liens, and a 2026 valuation in the typical Vienna range. Your actual figure will vary based on principal paid down, lot, condition, and submarket.

The other variable that matters more in Vienna than in most NOVA submarkets: school-zone premiums. Homes in the Madison HS pyramid (22181) and the prime portions of the Marshall and Oakton pyramids consistently command stronger pricing and faster days-on-market than comparable inventory just outside those boundaries. If you have been in your home for five-plus years and you are zoned for a top high school, your equity position is almost certainly stronger than a generic appreciation curve suggests.

The Three Primary Ways to Access Equity

Setting aside niche options like reverse mortgages (Vienna age 62+), home equity investments, and shared-appreciation products, almost every Vienna homeowner's decision comes down to three real choices:

| Option | What It Is | Equity Accessed | Keep Home? |

|---|---|---|---|

| HELOC | Revolving credit line secured by the home; you draw what you need, when you need it | Up to ~80–85% of value, minus first mortgage | Yes |

| Cash-Out Refinance | Replaces your existing mortgage with a new, larger one; you pocket the difference | Up to ~80% of value, minus payoff | Yes |

| Sell | List the home, close the sale, receive net proceeds at settlement | 100% of equity (minus closing costs and commissions) | No |

Relative cost of accessing $200,000 in equity

The chart below estimates the all-in cost — interest, closing fees, taxes, commissions — of pulling $200K out of a Vienna home through each path. These are illustrative ranges, not quotes; your actual cost depends on rate environment, lender, and home value.

*Sale costs include listing-side commission, buyer-agent compensation, Virginia grantor tax, recording fees, and standard settlement charges on a typical Vienna sale price. The sale path also unlocks all remaining equity, not just the $200K, which is part of why it looks comparatively efficient.

Option 1 — HELOC: How It Works in Vienna

A Home Equity Line of Credit is a second mortgage structured as a revolving credit line. The lender approves you for a maximum credit limit based on your home's appraised value and your existing first mortgage balance. You draw against the line as needed, pay interest only on what you actually borrow, and your first mortgage stays untouched.

For Vienna homeowners with low-rate first mortgages from 2020–2021 (3.0%–3.5% range), this is often the most attractive choice — you don't trade away that historically low payment.

Typical Vienna HELOC parameters

What to expect from a Vienna-area HELOC

- Maximum combined LTV: Usually 80%–85% of home value (combined first mortgage plus HELOC). On a $1.2M Vienna home with a $400K first mortgage, that means a HELOC up to roughly $560K–$620K.

- Interest rate: Variable, tied to Prime Rate plus a margin (commonly Prime + 0.5% to Prime + 2.0%, depending on credit profile and CLTV).

- Draw period: Typically 10 years where you can borrow and pay interest only.

- Repayment period: Usually 15–20 years after the draw period ends, with principal + interest payments.

- Closing costs: Often $0–$1,500; many lenders waive most fees on HELOCs.

- Underwriting: Income, employment, credit score (typically 680+), and a current appraisal or AVM.

When a HELOC makes sense

| ✓ Good Fit | ✗ Poor Fit |

|---|---|

| You have a sub-4% first mortgage you don't want to lose | You need a fixed payment for budgeting certainty |

| You need flexible access (renovation, tuition, business, bridge financing) | You will use 100% of the line on day one for a long-term purpose |

| You can stomach payment fluctuations as Prime moves | You're at the edge of your DTI ratio already |

| You want to keep the option to draw later without re-applying | You plan to sell the home within 12–24 months anyway |

⚠️ Variable-rate risk

HELOC rates move with Prime. A line drawn at 8% can become 10% or 11% if the Fed raises rates again. Stress-test your payment at Prime + 3% before committing — and avoid using a HELOC for non-recoverable expenses like vacations or consumer goods.

Option 2 — Cash-Out Refinance: When the Math Works

A cash-out refinance pays off your existing mortgage and replaces it with a new, larger one. You take the difference home in cash. The new loan is typically a 30-year fixed-rate first mortgage, and your old rate goes away — which is the central trade-off for most Vienna homeowners.

If you locked a 3.0% mortgage in 2021 and current 30-year fixed rates are at 6.75%, refinancing to extract $200K means you are paying that 6.75% on the entire balance — not just the new $200K. That is the math that has made cash-out refinances unattractive for many Vienna owners through 2023, 2024, and into 2026.

When the cash-out refi math works in 2026

Refinance becomes attractive when…

- Your existing rate is at or above current market rates (you're not giving up a low payment).

- You want the certainty of a fixed payment instead of HELOC variability.

- You need to access a large lump sum and plan to keep the home for at least 5–7 more years (long enough to amortize closing costs).

- You are consolidating high-interest debt where the rate spread is large enough to offset closing costs.

- You are using cash-out as part of a divorce buyout or estate equalization.

Cash-out refi rarely makes sense when…

- Your current rate is meaningfully below today's market rate.

- You only need a small amount of cash relative to your loan balance.

- You plan to sell within 3 years (you'll likely never recover the closing costs).

- You need the flexibility to draw and repay multiple times — that's HELOC territory.

- You'd be tapping equity for a non-essential or short-term purpose.

Cash-out refi closing costs in Vienna (typical)

| Cost Category | Typical Range | Notes |

|---|---|---|

| Lender origination + underwriting | $1,500–$4,000 | Varies by lender |

| Appraisal | $650–$900 | Vienna properties often appraise higher fee |

| Title insurance + settlement | $1,800–$3,500 | Scales with loan size |

| Recording + Virginia grantor tax | ~$0.25 per $100 of new loan | Refis pay state recordation tax on increase |

| Discount points (optional) | 0–2% of loan | Buy down the rate |

| Total closing costs | ~2–4% of new loan | $15K–$30K on a $750K refi is typical |

Option 3 — Selling Your Vienna Home

Selling is the most overlooked equity-access strategy — partly because most homeowners frame the conversation around financing rather than around their underlying goal. But if your real objective is to right-size, relocate, retire somewhere lower-cost, fund a major life event, or simply convert paper gains into real money, a sale unlocks 100% of your equity in a single transaction. No interest. No payment for life. No second lien on the title.

The trade-off is straightforward: you no longer own the home. For some Vienna homeowners that is exactly what they want — empty nesters whose kids have aged out of the Madison or Marshall pyramid, retirees considering Florida or the Carolinas, families upsizing into Great Falls or McLean, or owners who need the full equity for a non-housing purpose.

What selling actually costs in Vienna

Vienna sale costs follow a predictable structure. The largest variable is the listing-side commission, which is where The Jamil Brothers' 1.5% full-service listing program changes the equity math significantly. On a $1.2M Vienna sale, that's a difference of roughly $18,000 between a 1.5% fee and a traditional 3% fee — money that stays in the seller's pocket at settlement.

| Cost | Traditional 3% Listing | Jamil Brothers 1.5% |

|---|---|---|

| Listing-side commission | $36,000 | $18,000 |

| Buyer-agent compensation (negotiable, typical 2–2.5%) | $24,000–$30,000 | $24,000–$30,000 |

| Virginia grantor tax (~$0.25/$100) | ~$3,000 | ~$3,000 |

| NOVA regional WMATA tax (~$0.10/$100) | ~$1,200 | ~$1,200 |

| Settlement, recording, HOA transfer (varies) | $1,500–$3,000 | $1,500–$3,000 |

| Approx. total seller costs on $1.2M sale | ~$66K–$73K | ~$48K–$55K |

The 1.5% listing program is full-service. Professional photography, drone video, 3D tours, full MLS syndication, expert negotiation, and partner-led representation through closing are all included — same scope of marketing and service you would expect from a 3% listing, structured at a more efficient fee. You can see exactly what's included in the 1.5% listing program.

Get a personalized home valuation from The Jamil Brothers — Vienna street-level comps from 22180/22181/22182, not automated estimates. Response within 24 hours.

Side-by-Side Comparison: HELOC vs. Refi vs. Sale

Use this matrix as a fast diagnostic. None of these options is universally "better" — the right answer depends on your underlying goal.

| Factor | HELOC | Cash-Out Refi | Sell |

|---|---|---|---|

| How much equity unlocked | Up to ~80–85% CLTV | Up to ~80% LTV | 100% (minus costs) |

| Affects first mortgage | No | Yes — replaced | Paid off at closing |

| Rate type | Variable (Prime-based) | Fixed (typical) | N/A |

| Closing costs | $0–$1,500 | 2–4% of new loan | ~4–6% of price (lower with 1.5%) |

| Speed | 2–4 weeks | 3–6 weeks | Avg. 30–60 days list-to-close |

| Monthly payment impact | Adds new payment | New (often higher) payment replaces old | Eliminates payment entirely |

| Tax treatment of interest | Deductible if used to "buy, build, or substantially improve" home | Deductible up to $750K combined acquisition debt; cash-out portion subject to use-test | N/A — gain may qualify for $250K/$500K exclusion |

| Reversible? | Yes — pay back | Partially — refi again later | No |

Vienna Sale Net Proceeds Calculator

If selling is on the table, this calculator shows exactly how much more you keep with the 1.5% full-service listing program versus a traditional 3% agent. Vienna sales typically fall in the $750K–$1M+ range, but the calculator scales across price points so you can see your specific scenario.

Savings Calculator

How much more do you keep with our 1.5% listing fee?

Select your home's estimated value to see your real net proceeds — side by side. Vienna defaults to $1M based on local pricing.

Traditional Agent — 3%

Our Fee — Only 1.5%

Extra in your pocket

$6,000

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

Our Fee — Only 1.5%

Extra in your pocket

$7,500

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

Our Fee — Only 1.5%

Extra in your pocket

$9,000

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

Our Fee — Only 1.5%

Extra in your pocket

$11,250

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

Our Fee — Only 1.5%

Extra in your pocket

$15,000

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Estimates only. Closing costs vary. Buyer's agent commission is negotiable post-NAR settlement.

Our seller net sheet calculator breaks down every cost — commission, transfer taxes, settlement fees — so you know your real Vienna bottom line before you list.

Tax Implications You Need to Understand

Tax treatment is where many Vienna homeowners discover that the option that looks cheapest is not actually cheapest after-tax — and where the sale option, in particular, often turns out to be more attractive than expected.

The $250K / $500K primary-residence exclusion

Under IRC Section 121, single filers can exclude up to $250,000 of capital gain from the sale of a primary residence, and married couples filing jointly can exclude up to $500,000 — provided you have owned and lived in the home as your primary residence for at least 2 of the last 5 years. For a Vienna couple who bought in 2015 for $700K and sells today for $1.3M, that's a $600K gross gain — of which $500K is fully excluded from federal capital-gains tax. The remaining $100K is taxed at long-term capital gains rates (typically 15%–20%, depending on AGI).

This exclusion is one of the most powerful tax breaks in the U.S. tax code. It is also one of the most important reasons selling sometimes makes more sense than refinancing or HELOC'ing — you are converting equity to cash without triggering tax on the lion's share of the gain.

HELOC and cash-out refi interest deductibility

Since the Tax Cuts and Jobs Act (2017), HELOC and cash-out refinance interest is only deductible if the borrowed funds are used to "buy, build, or substantially improve" the home that secures the loan, and only up to the $750,000 combined acquisition-debt cap. If you HELOC $200K to consolidate credit card debt or pay tuition, that interest is not deductible. If you HELOC $200K for a kitchen-and-primary-suite renovation on the same home, the interest generally is deductible, subject to the cap.

ℹ️ Talk to a CPA

This is a real-estate guide, not a tax opinion. Capital gains, deduction phaseouts, AMT exposure, and Virginia state tax interact in ways that depend on your specific return. Run your scenario by a licensed CPA before pulling the trigger on any equity-access strategy.

Five Common Scenarios — Which Option Fits

1. Renovation funded by equity

Best fit: HELOC. You don't need all the money on day one, draws are tied to contractor milestones, and interest is potentially deductible since the funds are used to substantially improve the home. Vienna homeowners doing kitchens, primary suites, and basement finishes typically draw $80K–$250K against a HELOC over 6–18 months.

2. Empty-nest downsize

Best fit: Sell. A Vienna couple whose children have aged out of Madison or Marshall typically does not need 4,200 finished square feet anymore. Selling unlocks 100% of equity, eliminates the mortgage payment, and the $500K married-filing-jointly exclusion shields most of the gain. Many empty-nesters relocate to Reston, Tysons condos, or out of state with significant cash on hand after closing.

3. Divorce equalization

Best fit: Sell or cash-out refi (depending on custody and income). If neither spouse can refinance solo into a new mortgage at current rates, a sale is often the cleanest path. If one spouse plans to remain in the home (often for school continuity), a cash-out refi to buy out the other spouse's share is the typical mechanism. The Jamil Brothers handle divorce listings discreetly across Northern Virginia.

4. Funding a second home or investment property

Best fit: HELOC or cash-out refi. If you want to keep the Vienna home as a long-term hold and use equity to buy a beach house, mountain place, or rental, financing is the right tool. Note that interest on equity used for non-residence purposes is generally not deductible — but the math can still work depending on the investment return.

5. Retirement liquidity event

Best fit: Sell. If the goal is to fund a 25-year retirement, converting paper equity to a diversified portfolio almost always makes sense. Living off HELOC draws in retirement is dangerous — variable rates, ongoing payments, and the home still ties up most of your net worth. Selling, downsizing or relocating, and reinvesting the proceeds is the cleaner play.

Professional photography, drone video, 3D tours, expert negotiation, and full MLS marketing — all included at 1.5%. No hidden fees, no service reductions, no surprises.

Mistakes to Avoid When Tapping Equity

Common Vienna equity-access mistakes

- Refinancing out of a sub-4% rate without a clear long-term plan. If you're going to sell within 3 years anyway, you've burned closing costs and traded down on rate for nothing.

- Maxing out a HELOC at variable rates. A line drawn at 8% can become 11% in a tightening cycle. Never assume rates stay where they are.

- Underestimating sale costs by ignoring NOVA-specific transfer taxes. Virginia grantor tax and the NOVA WMATA congestion tax add roughly 0.35% on top of commissions and standard settlement charges.

- Listing with the first agent who says "I sold a home in your neighborhood" — without comparing fees and full-service scope. The fee difference between 3% and 1.5% on a Vienna sale is real money.

- Pulling equity to invest in volatile assets. Your home is collateral. If the investment loses value, the loan doesn't disappear.

- Forgetting the $250K/$500K capital gains exclusion has a 2-of-5-year rule. Convert your home to a rental and lose the primary-residence treatment if you don't sell within 3 years.

- Skipping a CPA or financial advisor consult. Tax math on $300K+ equity events deserves professional review.

How to Choose the Right Path

The right equity-access strategy follows a sequence of questions, not a default answer. Walk through these in order:

Define the goal — not the tool.

"I need $200K to renovate" is a different goal than "I want to retire and stop having a mortgage." The tool follows the goal.

Inventory your current mortgage rate, balance, and payoff.

If you have a sub-4% rate and only need partial liquidity, refinancing is almost always the wrong move.

Get a real Vienna valuation, not a Zestimate.

AVMs are notoriously inaccurate in Vienna's high-end submarkets. A street-level valuation from a working agent gives you the actual number you need to plan against.

Run all three numbers — HELOC payment, refi payment, and net-of-sale proceeds.

A net sheet from a listing agent and rate quotes from two lenders will tell you exactly what each option costs.

Layer in the tax math.

$500K of excluded gain is meaningful. So is non-deductible HELOC interest. Have your CPA model the after-tax outcome, not the gross numbers.

Choose, then move.

Equity decisions tend to drift. If a sale is the right answer, get on the market while inventory is favorable. If a HELOC is the right answer, lock the line while rates and limits are workable.

Frequently Asked Questions

How much equity do I need to qualify for a HELOC in Vienna?

Most lenders require at least 15%–20% equity in the home (an 80%–85% combined loan-to-value ratio) plus a credit score of 680+ and documented income. On a $1.2M Vienna home with a $400K first mortgage, you have roughly $800K of standalone equity, which translates to a HELOC limit somewhere between $560K and $620K depending on the lender's CLTV cap. Vienna's high property values make HELOCs particularly accessible compared to lower-priced submarkets.

Will a cash-out refinance hurt my credit score?

The hard credit pull during application typically drops your score by 5–10 points temporarily. Once the new mortgage reports, the impact depends on your overall credit profile — a larger balance can hurt your utilization picture, while on-time payments help. Most homeowners see their score recover within 6–12 months. A more significant credit-related risk is taking on a payment you cannot comfortably afford long-term.

How long does it take to sell a home in Vienna?

Vienna days-on-market varies by season, school zone, and price band, but most well-prepared, properly-priced Vienna homes go under contract within 14–30 days, with closing roughly 30 days after that. Homes in the Madison and Marshall pyramids consistently move faster than the broader Fairfax County average. Total list-to-close timeline of 45–60 days is realistic in a normal market.

What's the difference between a HELOC and a home equity loan?

A HELOC is a revolving credit line — you draw what you need over time and pay interest only on the drawn balance. A home equity loan (sometimes called a "second mortgage") is a one-time lump sum at a fixed rate with fixed monthly principal-and-interest payments. HELOCs are flexible but variable-rate. Home equity loans are predictable but give you all the money on day one — and you start paying interest on all of it immediately.

Can I avoid capital gains tax when I sell my Vienna home?

If the home has been your primary residence for at least 2 of the last 5 years, single filers can exclude up to $250,000 of capital gain and married couples filing jointly can exclude up to $500,000 under IRC Section 121. Above those thresholds, gain is taxed at long-term capital gains rates (typically 15%–20%). Most Vienna homeowners with 5+ years of ownership and standard improvements end up with most or all of their gain shielded by the exclusion. Always confirm with a CPA.

How does the post-NAR settlement affect Vienna home sales?

Following the August 2024 NAR settlement, buyer-agent compensation is no longer presumed to be paid by the seller and is no longer advertised in the MLS. Sellers and buyer agents now negotiate buyer-side compensation as part of the offer, often through a written buyer-broker agreement. In practice, most Vienna sellers continue offering 2%–2.5% to buyer agents, but the structure is more transparent and negotiable than before. The Jamil Brothers' 1.5% listing fee covers the listing-side commission only — buyer-side compensation is structured separately on each transaction.

What does the Jamil Brothers' 1.5% listing program actually include?

The 1.5% full-service listing program includes professional 4K photography, drone video, 3D Matterport tours, full MLS syndication across BrightMLS and aggregator sites (Zillow, Realtor.com, Redfin), professional staging consultation, expert negotiation by Saad and Arslan personally, and management of the entire transaction through closing. It is structurally identical in scope to a 3% listing — the difference is in the fee, not the service. The Jamil Brothers Realty Group has closed 840+ homes and over $500M in volume across the DMV.

Should I tap equity to pay off credit card debt?

The math sometimes works — converting 22% credit-card APR debt to a 9% HELOC saves real money on interest. But the risk profile changes significantly: unsecured credit card debt becomes secured debt against your home. If you cannot make payments, you can lose the house. Most financial advisors recommend tapping equity for debt consolidation only when paired with a plan that addresses the underlying spending pattern. Otherwise, you risk running the cards back up while still carrying the home equity loan.

Are HOA transfer fees a factor when selling in Vienna?

Many Vienna subdivisions and townhome/condo communities charge HOA disclosure-package fees and transfer/resale fees that range from $200 to over $1,000 combined. Single-family homes in non-HOA portions of Vienna (much of the older town center) avoid these fees entirely. Your Jamil Brothers listing agent handles the HOA package ordering and ensures fees are disclosed correctly on the settlement statement.

What's the best time of year to sell in Vienna?

Vienna sales activity peaks from mid-March through June, with a secondary window from September through early November. Spring listings benefit from school-zone driven family demand — buyers want to be in the Madison or Marshall pyramid before the next school year starts. That said, well-priced Vienna inventory sells year-round, and lower winter inventory often means less competition. The Jamil Brothers can help you map the right list date to your specific home's profile.

Can I sell while still carrying a HELOC?

Yes. The HELOC is paid off at closing as part of the standard settlement process, just like the first mortgage. The HELOC payoff comes out of your gross sale proceeds before you receive your net check. You don't need to pay it down before listing — your settlement attorney handles the payoff order with the lender. Make sure your listing agent factors the current HELOC balance into your net sheet.

How do I pick the right Vienna listing agent?

Evaluate Vienna agents on objective criteria: total transactions in Vienna ZIPs (22180/22181/22182) over the last 24 months, average list-to-sale price ratio, average days on market versus the local average, marketing scope (professional photography, drone, 3D tours), and fee structure. Verify they are licensed in Virginia and ask for their NVAR designation status. The Jamil Brothers Realty Group has closed 840+ homes across Northern Virginia, holds NVAR Lifetime Top Producer status, and operates under Samson Properties — and the 1.5% full-service listing program lets Vienna sellers keep meaningfully more of their equity at closing.

Glossary

HELOC

Home Equity Line of Credit — a revolving credit line secured by your home, with variable interest rate tied to Prime.

Cash-Out Refinance

A new mortgage that replaces your existing one for a larger amount; you receive the difference in cash at closing.

CLTV

Combined Loan-to-Value ratio — total of all mortgages and liens on the home divided by the home's appraised value.

Section 121 Exclusion

IRS rule allowing exclusion of $250K (single) / $500K (married filing jointly) of capital gain on the sale of a primary residence.

Grantor Tax

Virginia state seller-paid transfer tax of approximately $0.25 per $100 of sale price, plus regional WMATA tax in NOVA.

Net Proceeds

The actual cash a seller receives at closing — sale price minus mortgage payoff, commissions, taxes, and settlement costs.

Draw Period

The phase of a HELOC (typically 10 years) during which you can borrow against the line and pay interest only on drawn amounts.

Prime Rate

A benchmark interest rate that banks use as a reference for HELOCs and other variable-rate consumer loans.

Putting It All Together

Vienna homeowners in 2026 are sitting on a stronger equity position than most NOVA submarkets — and that creates real options. A HELOC keeps your low-rate first mortgage intact and gives you flexible draws. A cash-out refinance makes sense when current rates are favorable and you want fixed-payment certainty. A sale unlocks 100% of your equity in a single transaction, and with the $500K married-couple capital-gains exclusion plus the 1.5% full-service listing fee, the after-tax-after-cost outcome is often more attractive than homeowners initially expect.

The right answer is the one that matches your actual goal — renovation, downsize, retirement, divorce, second home, or simply converting paper gains to liquid capital. Run the numbers on all three before you decide.

Know your equity, understand your costs, and see exactly what you'll walk away with — before you make any decisions. The Jamil Brothers provide a full seller consultation at no cost or obligation.

Explore More Northern Virginia Guides

Vienna McLean Fairfax Reston Herndon Ashburn 1.5% Listing Program Seller Net Sheet Free Home Valuation Cash OffersThe Jamil Brothers Realty Group · Samson Properties · (703) 782-4830 · Licensed in Virginia, Maryland, Washington D.C., and West Virginia

Explore More

Browse Every Corner of the DMV Market

Whether you're searching by budget, neighborhood, or buying situation — find exactly what you need below.

Virginia Homes by Budget

Washington DC Homes by Budget

Maryland Homes

Explore Northern Virginia Communities

Loudoun County

Fairfax County & Surrounding

Ready to Make a Move?

Full-Service · No Tradeoffs

List for 1.5% & Keep More Equity

Professional photography, drone video, 3D tours, and expert negotiation — all included. On an $800K home, that's $12,000 more in your pocket vs. a 3% agent.

See the 1.5% Program →Need Speed or Certainty?

Get a No-Obligation Cash Offer

Skip the showings, skip the contingencies. If timing or condition matters more than top dollar, a cash offer may be the right fit. We'll walk you through every option.

Explore Cash Offers →Categories

Recent Posts

Let's Connect