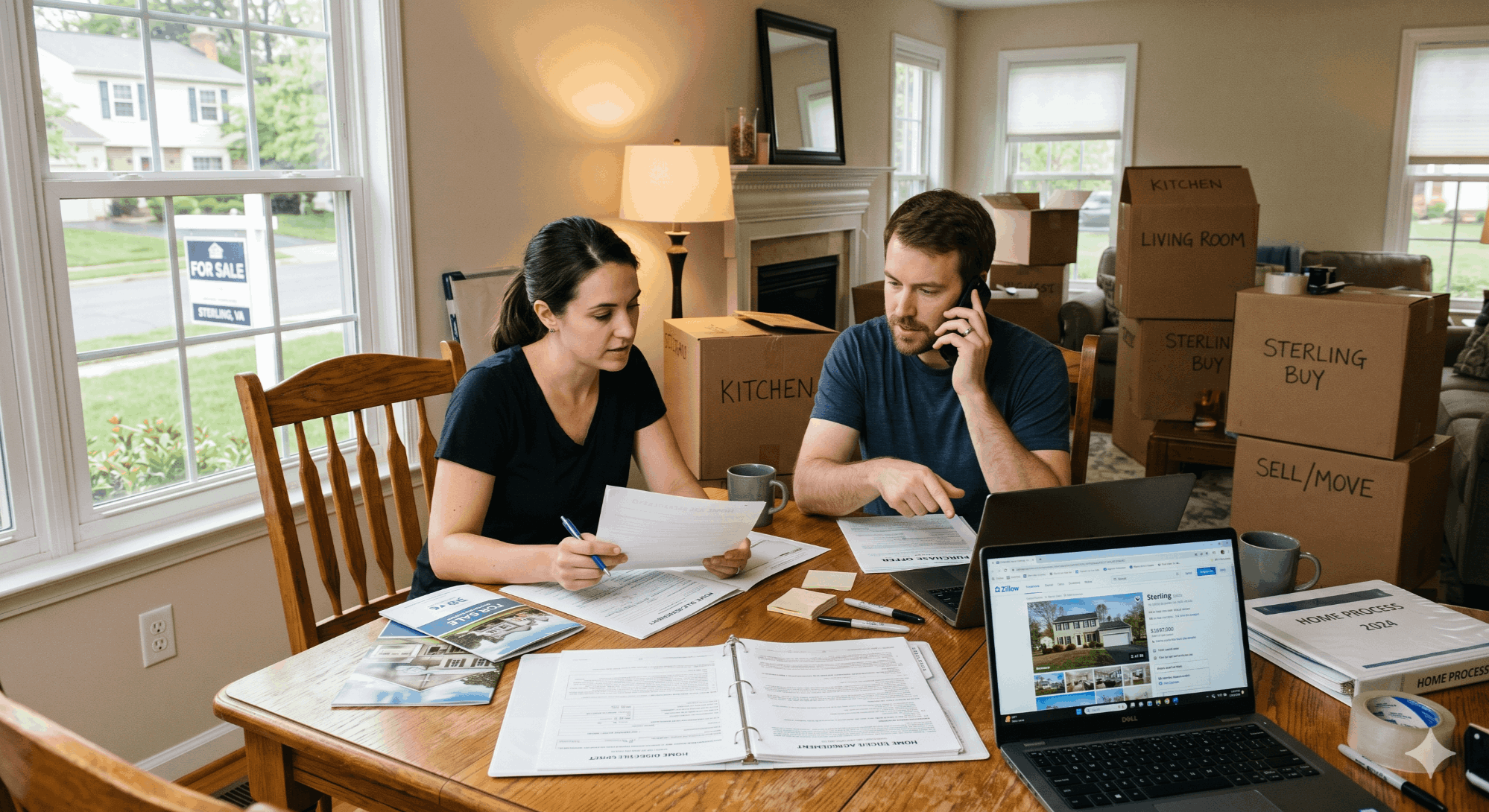

How to Sell and Buy a Home at the Same Time in Sterling, VA

Selling your current Sterling home and buying your next one at the same time is one of the trickiest moves in Northern Virginia real estate. In a Loudoun County market where well-priced homes still sell in under three weeks but multi-offer scenarios are no longer guaranteed, you have to coordinate two transactions, two financing pieces, and two closing tables — without ending up homeless, double-mortgaged, or forced to accept a low offer because the clock ran out. This guide walks you through every option Sterling sellers actually use in 2026, the real costs of each, and how to choose the right path for your situation.

Quick Answer: Most Sterling sellers buying and selling at the same time choose one of three paths: (1) sell first with a rent-back, (2) buy first using a bridge loan or HELOC, or (3) write a sale-contingent offer. With Loudoun County median sale prices in the high-$700Ks and average days on market around 12–18 days for well-prepared homes, sell-first with a 30–60 day rent-back is the most common choice — it eliminates double-mortgage risk while still giving you time to close on your next property.

Key Takeaways

- Sterling's median sale price sits in the high-$700Ks in 2026, with townhomes from the $500Ks and single-family detached homes in Cascades, Lowes Island, and Potomac Falls clearing $900K+.

- Six strategies exist — sell-first with rent-back, buy-first with bridge loan, HELOC-funded down payment, sale-contingent offer, simultaneous close, and cash offer — each with different risk and cost profiles.

- The biggest financial risks are double-mortgage exposure (if you buy first and your home doesn't sell) and short-term housing costs (if you sell first without a rent-back).

- With our 1.5% full-service listing program, the average Sterling seller keeps an extra $9,000–$15,000 in equity — money that can fund the down payment on the new home or cover bridge financing costs.

- The single biggest mistake is starting the buy side before you have a market-tested list price on your current Sterling home.

In This Guide

- Sterling Market Snapshot (2026)

- The Two Big Risks of Doing Both at Once

- Six Sell-and-Buy Strategies in Sterling

- Decision Framework: Which Path Fits You

- Cost Side-By-Side: Buy First vs Sell First

- Seller Savings Calculator

- Step-By-Step Sterling Sell-and-Buy Timeline

- Coordinating the Two Closings

- Sterling Closing Costs Breakdown

- Common Mistakes to Avoid

- How to Choose the Right Agent

- Your Next Steps

- Frequently Asked Questions

- Glossary

For Sterling homeowners, the simultaneous sell-and-buy isn't a fringe scenario — it's the default. Most families moving up from a Sugarland Run townhouse to a Cascades single-family, or downsizing from Lowes Island into a Potomac Falls patio home, have to do both transactions in a tight window. The mistake is treating them as two separate problems instead of one coordinated plan.

The good news is that Sterling's location makes timing more manageable than most NOVA markets. With access to the Silver Line, Dulles Toll Road, and Route 7, your buyer pool extends from Reston commuters to Loudoun families to Maryland transplants — meaning a well-priced Sterling listing rarely sits. And on the buy side, you have inventory across Loudoun County, Western Fairfax, and even Frederick County to work with. The challenge is sequencing, not demand.

Sterling Market Snapshot (2026)

Before you decide on a sell-and-buy strategy, anchor your plan to the current Sterling market. Median sale prices, average days on market, and list-to-sale ratios drive everything else — including whether a sale-contingent offer has any chance of being accepted.

| Sterling Sub-Market | Typical Price Range | Median DOM | List-to-Sale |

|---|---|---|---|

| Sterling Park (older single-family) | $575K–$725K | 14–20 days | 99–101% |

| Sugarland Run (townhomes & SFH) | $525K–$775K | 12–18 days | 99–102% |

| Countryside | $575K–$825K | 10–16 days | 100–102% |

| Cascades | $725K–$1.1M | 10–15 days | 100–103% |

| Lowes Island / Potomac Falls | $850K–$1.4M | 14–22 days | 99–102% |

| Sterling townhomes (overall) | $475K–$650K | 10–14 days | 100–102% |

Ranges reflect BrightMLS data trends for Sterling ZIP codes 20164, 20165, and 20166. Cascades and Lowes Island typically command a premium because of Potomac River proximity and Algonkian Regional Park access, while older Sterling Park homes appeal to buyers who want larger lots without HOA fees.

What this means for your sell-and-buy plan:

Because Sterling sells fast, sell-first strategies carry less timing risk than they would in a slower market. But because you'll be buying in the same Loudoun-Fairfax region with similar competition, buy-side leverage from a sale-contingent offer is limited — sellers in Ashburn, Leesburg, or Reston rarely accept contingent contracts when they have clean cash or conventional offers available.

The Two Big Risks of Doing Both at Once

Every sell-and-buy strategy is a trade-off between two financial risks. Understanding them upfront makes the rest of your decisions easier.

Risk 1: Double-Mortgage Exposure

If you close on your new home before your current Sterling home sells, you're carrying two mortgages, two sets of property taxes, and two HOA dues for however long the old home sits. On a $750K Sterling home with a $4,800 monthly payment, every extra month of overlap costs you roughly that much in burn — and that's before insurance and utilities. A bridge loan or HELOC can soften the cash-flow blow but adds origination fees and interest expense.

Risk 2: Short-Term Housing Gap

If you sell first without a rent-back and your next purchase falls through, gets delayed, or hasn't been identified yet, you need somewhere to live. That can mean an extended-stay hotel, a furnished short-term rental in Ashburn or Reston (typically $4,500–$7,500/month), or moving in with family. Storage, double moves, and lost time become real costs.

| ✓ Sell First Eliminates | ✗ But Buy First Eliminates |

|---|---|

| Double-mortgage risk | Short-term housing scramble |

| Bridge loan interest costs | Sale-contingent offer weakness |

| Uncertainty about your sale price (and equity) | Pressure to accept a lowball offer later |

| Carrying-cost stress | Moving twice or paying for storage |

Most Sterling sellers reduce both risks by combining sell-first with a 30–60 day rent-back from the buyer — but that only works when the local market supports it. We'll cover when it does and doesn't below.

Six Sell-and-Buy Strategies in Sterling

1. Sell First with a Rent-Back

You list and sell your Sterling home, then negotiate a 30–60 day post-closing occupancy (sometimes called a "use and occupancy" or U&O) with the buyer. You collect your sale proceeds at closing, then pay the buyer a daily occupancy fee — typically the buyer's PITI (principal, interest, taxes, insurance) divided by 30 — to stay in the home while you close on your next property.

Best for: Sellers who need cash from the sale to fund the next down payment, and who don't want double-mortgage risk.

2. Buy First with a Bridge Loan

A bridge loan is a short-term loan (typically 6–12 months) secured by your current Sterling home that gives you the down payment for the new one. After your Sterling home sells, the proceeds pay off the bridge loan. Rates are higher than conventional mortgages — usually 1.5–3 points above prime — and origination fees range from 1.5% to 2%. But it lets you make a non-contingent offer on the new home.

Best for: Sellers competing in a tight Ashburn, Leesburg, or Western Fairfax buy market where contingent offers won't be taken seriously.

3. HELOC-Funded Down Payment

A home equity line of credit (HELOC) on your current Sterling home gives you a flexible draw — you borrow only what you need for the down payment. Once your sale closes, you pay it off. Setup costs are usually $0–$500 and rates are tied to prime, so they fluctuate. Critical: the HELOC must be opened before you list — most lenders won't approve a HELOC on a property that's actively for sale.

Best for: Sellers with substantial Sterling equity (50%+ LTV available) who want a cheaper alternative to a bridge loan.

4. Sale-Contingent Offer

Your offer on the new home is contingent on selling your current Sterling home within a specified window (typically 30–60 days). If your home doesn't sell or go under contract in time, you can walk from the new purchase without penalty.

Reality check for Sterling buyers: in the current Loudoun-Fairfax market, sale-contingent offers are rarely competitive against clean offers. Use this strategy only for properties that have been sitting (30+ DOM), in slower price tiers, or when you have a strong listing pre-marketing report on your Sterling home to back the contingency.

5. Simultaneous Close

You schedule both closings for the same day — sometimes back-to-back at the same title company. Proceeds from the sale wire directly to fund the purchase. This eliminates double-mortgage risk and short-term housing risk but requires both transactions to be locked, clean, and ready. One delay (an appraisal issue, a buyer financing hiccup) on either side can cascade.

Best for: Sellers with experienced agents on both sides who can coordinate the lender, title company, and both contracts.

6. Cash Offer for the Current Home

You accept a cash offer (from an investor, iBuyer, or "we buy houses" company) on your Sterling home, then use the certainty of close to buy your next home without a contingency. Cash offers typically come in 5–15% below open-market value, so the savings on financing and timing have to outweigh the price haircut.

Best for: Sellers whose home needs significant repairs, who are time-constrained (relocation, divorce, inherited property), or who simply value certainty over maximum price.

| Strategy | Best When | Watch Out For |

|---|---|---|

| Sell-first + rent-back | You need sale equity to buy | Buyer financing must accept rent-back (most do, max 60 days) |

| Bridge loan | Buy-side competition is fierce | 2–3% in fees + higher interest rate |

| HELOC | You have strong equity, open BEFORE listing | Variable rate, can't open while listed |

| Sale-contingent offer | Target home has been sitting | Rarely accepted in hot price tiers |

| Simultaneous close | Both contracts are locked & clean | Any delay on either side cascades |

| Cash offer (sell side) | Speed or certainty > max price | 5–15% below open-market value |

Decision Framework: Which Path Fits You

The right strategy comes down to four questions. Answer them honestly and the path usually picks itself.

Sterling Sell-and-Buy Decision Checklist

- ✓ Do I need my Sterling sale proceeds to make the next down payment? If yes → sell-first or HELOC/bridge.

- ✓ Could I qualify for two mortgages temporarily? If yes → buy-first with bridge or HELOC opens up.

- ✓ How fast does my Sterling home likely sell? Use sub-market DOM (12–20 days for most areas) — short DOM = sell-first is low risk.

- ✓ Where am I buying? Hot markets (Ashburn, Reston, McLean) need non-contingent offers. Slower tiers tolerate contingency.

- ✓ How time-flexible am I? School calendars, work, family — rigid timing tilts toward simultaneous close or rent-back.

- ✓ What's my risk tolerance? Conservative = sell-first. Aggressive = buy-first with bridge.

Before you can sequence two transactions, you need a real number on your current home — not a Zestimate. Get a personalized Sterling valuation from The Jamil Brothers with street-level comps from Cascades, Sugarland Run, Lowes Island, and every Sterling sub-market. Response within 24 hours.

Cost Side-By-Side: Buy First vs Sell First in Sterling

Here's what each path actually costs on a typical Sterling scenario — a $750K current home and a $950K next home in Loudoun or Western Fairfax. Real numbers, not theoretical ones.

| Cost Category | Sell-First + Rent-Back | Buy-First + Bridge Loan | Simultaneous Close |

|---|---|---|---|

| Rent-back daily fee (30 days) | ~$4,500–$5,500 | $0 | $0 |

| Bridge loan origination (1.5–2%) | $0 | $3,500–$4,500 | $0 |

| Bridge interest (~3 months) | $0 | $4,500–$7,000 | $0 |

| Risk of carry costs if delay | Low | High ($4,800/mo) | Low |

| Short-term housing risk | Eliminated by rent-back | Eliminated | Eliminated |

| Typical total premium | $4,500–$5,500 | $8,000–$11,500 | $0 |

Note: A simultaneous close is "free" only if both transactions hold together. If yours doesn't and you have to scramble for housing or extend, the real cost can exceed bridge financing.

Notice what's missing from the cost table: your commission. The biggest single cost of selling — and the most controllable — is the listing fee. On a $750K Sterling sale, the difference between paying 3% and paying our 1.5% full-service listing fee is roughly $11,250. That savings can fund the bridge loan, the rent-back fees, or your moving budget — with money left over.

Sterling Sell-and-Buy Savings Calculator

How much more do you keep with our 1.5% listing fee?

Select your Sterling home's estimated value to see your real net proceeds — side by side.

Traditional Agent — 3%

| Sale price | $400,000 |

| Listing fee (3%) | −$12,000 |

| Buyer's agent (2.5%) | −$10,000 |

| Est. closing (1%) | −$4,000 |

Our Fee — Only 1.5%

| Sale price | $400,000 |

| Listing fee (1.5%) | −$6,000 |

| Buyer's agent (2.5%) | −$10,000 |

| Est. closing (1%) | −$4,000 |

Extra in your pocket

$6,000vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

| Sale price | $500,000 |

| Listing fee (3%) | −$15,000 |

| Buyer's agent (2.5%) | −$12,500 |

| Est. closing (1%) | −$5,000 |

Our Fee — Only 1.5%

| Sale price | $500,000 |

| Listing fee (1.5%) | −$7,500 |

| Buyer's agent (2.5%) | −$12,500 |

| Est. closing (1%) | −$5,000 |

Extra in your pocket

$7,500vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

| Sale price | $600,000 |

| Listing fee (3%) | −$18,000 |

| Buyer's agent (2.5%) | −$15,000 |

| Est. closing (1%) | −$6,000 |

Our Fee — Only 1.5%

| Sale price | $600,000 |

| Listing fee (1.5%) | −$9,000 |

| Buyer's agent (2.5%) | −$15,000 |

| Est. closing (1%) | −$6,000 |

Extra in your pocket

$9,000vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

| Sale price | $750,000 |

| Listing fee (3%) | −$22,500 |

| Buyer's agent (2.5%) | −$18,750 |

| Est. closing (1%) | −$7,500 |

Our Fee — Only 1.5%

| Sale price | $750,000 |

| Listing fee (1.5%) | −$11,250 |

| Buyer's agent (2.5%) | −$18,750 |

| Est. closing (1%) | −$7,500 |

Extra in your pocket

$11,250vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

| Sale price | $1,000,000 |

| Listing fee (3%) | −$30,000 |

| Buyer's agent (2.5%) | −$25,000 |

| Est. closing (1%) | −$10,000 |

Our Fee — Only 1.5%

| Sale price | $1,000,000 |

| Listing fee (1.5%) | −$15,000 |

| Buyer's agent (2.5%) | −$25,000 |

| Est. closing (1%) | −$10,000 |

Extra in your pocket

$15,000vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Estimates only. Closing costs vary. Buyer's agent commission is negotiable.

Step-By-Step Sterling Sell-and-Buy Timeline

Here's the realistic timeline most Sterling sellers follow when using the sell-first + rent-back strategy. Adjust by 2–3 weeks for buy-first paths.

Week 1–2: Pre-Listing Strategy & Valuation

Get a comparative market analysis on your Sterling home. Identify your target buy market (Ashburn, Brambleton, Western Fairfax, etc.) and run mortgage pre-qualification with the new payment scenario. Decide your strategy now — not after the listing goes live.

Week 3–4: Prepare to List

Decluttering, paint touch-ups, light staging, and pre-inspection if your home is 15+ years old. Professional photography, drone video, and 3D tour scheduled. If you're going the HELOC route, this is your last window to apply before listing.

Week 5: Go Live + Active Buy-Side Search

Listing hits BrightMLS Thursday evening or Friday morning. Begin viewing buy-side properties immediately, focusing on inventory that's been on market 10+ days (more contingency-friendly).

Week 5–7: Sterling Home Under Contract

Most well-marketed Sterling homes go under contract within 10–18 days. Negotiate a 30–60 day rent-back at this stage. Now your buy-side search becomes much more aggressive — you have a confirmed sale and a realistic close date.

Week 6–9: New Home Under Contract

With a ratified sale contract on your Sterling home, you can write strong offers on your new property. Match your buy-side close date to your sell-side close date plus the rent-back window. Lock financing immediately.

Week 8–10: Sell-Side Closing

Sterling home closes. You receive net proceeds (now your buy-side down payment). Rent-back kicks in — you stay in the home and pay the buyer's daily fee.

Week 10–14: Buy-Side Closing & Move

New home closes. You move out of Sterling rent-back home directly into the new property. One move, no storage, no temporary housing.

Before you write a single offer on the new home, run your full sell-side net sheet. Our calculator breaks down every Sterling closing cost — Virginia grantor tax, congestion tax, HOA transfer, recording fees — so you know your real bottom line before you list.

Coordinating the Two Closings (Bridge Loans, HELOCs, Rent-Backs)

The coordination layer is where most sell-and-buy deals get rocky. Here's how the pieces fit together.

Rent-Back Mechanics

Rent-backs are negotiated as part of the sale contract — a "Post-Settlement Occupancy Agreement" addendum in Virginia. Critical terms:

- Duration: Most lenders cap at 60 days. Anything longer triggers tenant/landlord regulations.

- Daily rate: Typically buyer's PITI ÷ 30. On a $750K Sterling sale, that's roughly $150–$185/day.

- Security deposit: Buyer usually holds 1% of sale price as damage deposit, refunded after move-out.

- Buyer financing: Conventional and VA loans typically permit rent-back up to 60 days. FHA loans are stricter — under 60 days only if the home is owner-occupied at closing.

- Insurance: Your homeowner's insurance must convert to renter's coverage at closing; buyer takes over the property insurance.

HELOC Timing

If you want to use a HELOC for your buy-side down payment, you must open it before you list your Sterling home. Lenders pull credit and an automated valuation when you apply, and most won't approve a HELOC on a property under active listing. Plan 4–6 weeks of lead time for HELOC underwriting. Once approved, the line stays open and unused until you need it.

Bridge Loan Mechanics

Bridge loans are secured by your current Sterling home and typically allow you to borrow up to 80% of its current equity. Once your home sells, the sale proceeds pay off the bridge in full. Watch for:

- Origination fees: 1.5–2% of loan amount.

- Interest rate: typically 2–3 points above prime, interest-only payments during the bridge period.

- Loan term: usually 6–12 months, but most close in under 90 days when the sale moves quickly.

- Prepayment penalty: confirm there isn't one — most don't have it, but verify.

Simultaneous Close Logistics

For a true simultaneous close, both contracts need to use the same (or coordinated) title company, both loans need to be clear-to-close at least 5 business days before settlement, and both closings should be scheduled the same morning — sell side first, buy side immediately after. The proceeds wire from your sale funds the buy-side closing directly. One delay anywhere — a last-minute repair credit dispute, an appraisal challenge — cascades to both closings.

Sterling Closing Costs Breakdown

When you sell and buy in Sterling, you pay closing costs on both sides. Here's what to expect on a $750K sell / $950K buy scenario in Loudoun County.

| Cost | Sell Side ($750K) | Buy Side ($950K) | Notes |

|---|---|---|---|

| Listing fee (JB 1.5%) | $11,250 | — | vs. $22,500 at 3% |

| Buyer's agent commission | $18,750 (often) | negotiable | Post-NAR, fully negotiable |

| VA grantor tax ($1 per $1K) | $750 | — | State transfer tax |

| NOVA congestion tax | $112 | — | $0.15 per $100, Loudoun applies |

| Title insurance (owner's) | — | $2,800–$3,400 | One-time, optional but standard |

| Recording & settlement fees | $600–$900 | $1,200–$1,600 | Loudoun County clerk fees |

| HOA / condo transfer | $300–$500 | $300–$500 | Cascades, Sugarland Run, Countryside |

| Property tax proration | Variable | Variable | Loudoun rate: ~1.045% of assessed value |

| Lender fees (origination, appraisal) | — | $2,500–$4,500 | Conventional loan |

ℹ️ Loudoun County Specifics

Sterling falls under Loudoun County jurisdiction. Real estate tax assessments are reset annually, and the 2026 rate is approximately $1.045 per $100 of assessed value. The NOVA regional congestion tax ($0.15 per $100) is paid by the seller and applies to all Loudoun, Fairfax, Arlington, Alexandria, Falls Church, and Manassas-area transactions.

4K photography, drone video, 3D tours, expert negotiation, full BrightMLS syndication, and partner-led representation — included at our 1.5% full-service listing fee. On a $750K Sterling home, you keep an extra $11,250 in equity compared to a traditional 3% listing.

Common Mistakes to Avoid

Sterling Sell-and-Buy: Six Mistakes That Cost the Most

- ✗ Touring buy-side homes before listing yours. You'll find your "dream home" before you know your sale price, then panic-buy with a weak contingent offer.

- ✗ Applying for a HELOC after listing. Most lenders won't approve a HELOC on an actively listed property. Apply 4–6 weeks before listing.

- ✗ Overpricing your Sterling home. A bad first 14 days creates a stale listing that buyers see as "what's wrong with it?" — destroying your negotiation leverage right when you need it for the buy side.

- ✗ Skipping the rent-back negotiation. In a sell-first plan, the rent-back is your buffer against short-term housing. Don't accept an offer that doesn't allow it.

- ✗ Using two different agents. One agent (or one team) running both sides catches timing conflicts a hand-off between two strangers never will.

- ✗ Ignoring carry costs. Every extra month of overlap on a $750K home costs roughly $4,800 in mortgage payments alone — that's your bridge loan budget being burned.

If timing matters more than maximum price — relocation, divorce, inherited Sterling property, or a buy-side opportunity that won't wait — a cash offer on your current home gives you certainty of close. We'll walk you through every option, including open-market sale vs. cash, side by side. No pressure.

How to Choose the Right Agent for a Sterling Sell-and-Buy

When you're handling two transactions at once, agent skill compounds — a small mistake on either side hurts the other. Use these objective criteria when interviewing:

Sterling Sell-and-Buy Agent Checklist

- ✓ Has closed 25+ Loudoun County transactions in the last 24 months. Local volume = local lender, title, and inspector relationships.

- ✓ Can run both sides of the transaction. One agent or one team. Hand-offs between disconnected agents create dropped balls.

- ✓ Provides marketing samples. Photography, drone, 3D tour — request to see the actual deliverables, not slides about them.

- ✓ Reviews from sellers, not just buyers. Google, Zillow, Realtor.com — filter for "sold by" reviews.

- ✓ Walks you through a written net sheet — before signing anything. Numbers should be clear, itemized, and locked in writing.

- ✓ Full-service at a reasonable fee. The right comparison isn't 3% vs. 1% — it's full-service vs. limited-service. Make sure marketing, negotiation, and full representation are included.

The Jamil Brothers Realty Group has closed 840+ homes in the DMV across both sides of more than 200 sell-and-buy transactions. We're NVAR Lifetime Top Producers, top 1% nationwide, and our full-service listing program lists Sterling homes at 1.5% — with professional photography, drone video, 3D tours, partner-led negotiation, and full BrightMLS syndication included. Phone: (703) 782-4830.

Your Next Steps

If you're planning a Sterling sell-and-buy in the next 3–9 months, the highest-leverage moves you can make right now are:

- Get a real valuation on your Sterling home. Not a Zestimate. A walk-through and a written CMA with closed-comp evidence. This is the number that drives every other decision.

- Run your full net sheet at multiple price scenarios. Understand exactly what you'll walk away with at the conservative, market, and aggressive list price.

- Pre-qualify for the new mortgage with two scenarios: assuming current Sterling mortgage stays in place (buy-first) and assuming it's gone (sell-first).

- Open the HELOC if you're using one. Apply now — before any listing activity.

- Map your target buy area. Ashburn, Brambleton, Reston, Western Fairfax, Frederick County — each has different timing, price, and contingency dynamics.

- Choose your strategy and lock your agent. One team, two transactions, one coordinated plan.

Sterling sits at a strategic crossroads in the DMV — close enough to the Silver Line and Reston to attract Northern Virginia commuters, and far enough into Loudoun to give you single-family inventory at prices Fairfax can't match. When you sell here right, you're not just exiting a property — you're funding the next chapter. Done well, the whole thing happens in 10–14 weeks with one move, no scramble, and the maximum equity intact.

Know your Sterling equity, understand your closing costs, and see exactly what you'll walk away with — before you make any decisions. The Jamil Brothers provide a full sell-and-buy consultation at no cost or obligation.

Explore More Sterling & Loudoun Guides

Sterling Ashburn Leesburg Herndon Reston 1.5% Listing Program View Loudoun HomesFrequently Asked Questions

Should I sell my Sterling home first or buy first?

For most Sterling sellers in 2026, sell-first with a 30–60 day rent-back is the lowest-risk option. It eliminates double-mortgage exposure, gives you your real sale equity for the next down payment, and the rent-back covers your short-term housing gap. Buy-first with a bridge loan or HELOC makes sense only if you have strong cash reserves, the buy market is highly competitive (Ashburn, McLean, Reston in hot tiers), and your Sterling home is expected to sell within 30 days based on current comps.

How much does it cost to sell and buy at the same time in Sterling?

On a $750K sell / $950K buy scenario, total closing costs typically run $40,000–$55,000 combined, depending on the strategy chosen. Sell-side costs include the listing fee (1.5% with The Jamil Brothers vs. 3% traditional, saving roughly $11,250), buyer's agent commission (post-NAR settlement, fully negotiable), Virginia grantor tax ($750 at this price), NOVA congestion tax (~$112), HOA transfer fees ($300–$500), and recording fees ($600–$900). Buy-side costs typically add $5,000–$8,000 in lender fees, title insurance, and recording. Bridge financing adds $8,000–$11,500 if used.

How long does a sell-and-buy transaction take in Sterling?

A typical Sterling sell-and-buy with the sell-first + rent-back strategy takes 10–14 weeks from initial listing prep to final move-in. That breaks down as: 2 weeks pre-listing prep, 1 week active listing to contract, 4–5 weeks sell-side under contract to close, 30–60 days rent-back, and 4–6 weeks for buy-side close (often overlapping with the rent-back). Buy-first strategies typically run 12–16 weeks because the listing has to happen during the bridge financing window.

Can I use the same agent for both my Sterling sale and new purchase?

Yes — and you should. Using one agent or one team for both transactions is the single biggest predictor of a smooth sell-and-buy timeline. One coordinator catches conflicts between the two closing dates, manages communication with both lenders and title companies, and prevents the hand-off problems that cause delays. The Jamil Brothers Realty Group runs both sides of more than 200 sell-and-buy transactions across the DMV, including dozens in Sterling and broader Loudoun County.

What is a rent-back and how does it work in Virginia?

A rent-back (formally called a Post-Settlement Occupancy Agreement in Virginia) is a contract addendum that lets the seller stay in the home for an agreed number of days after closing in exchange for a daily fee paid to the new owner. The fee is typically calculated as the buyer's principal, interest, taxes, and insurance divided by 30. Conventional and VA loans typically allow up to 60 days; FHA loans are stricter. The seller must convert homeowner's insurance to renter's insurance at closing.

Do sale-contingent offers work in Sterling's current market?

Sale-contingent offers are rarely competitive in Sterling, Ashburn, Reston, or Loudoun's hot tiers right now. Sellers in those areas typically receive clean conventional or cash offers and have no reason to accept a contingency. Where contingent offers work better is on Loudoun properties that have been sitting on market for 30+ days, in higher price tiers ($1.4M+) where buyer pools are smaller, and in specific situations where the seller is also doing a sell-and-buy and needs flexibility.

What happens to my Sterling HOA dues during the rent-back period?

After closing, the new buyer is the legal owner and is responsible for HOA dues, property taxes, and homeowner's insurance. The seller (now occupant during rent-back) pays only the daily occupancy fee, renter's insurance, and utilities. Sterling HOA-governed neighborhoods like Cascades, Sugarland Run, Countryside, and Lowes Island all permit standard rent-back arrangements without HOA notification or additional fees in most cases — confirm with your specific community manager.

How much equity do I need to use a bridge loan?

Most bridge loans require at least 30% equity in your current Sterling home — typically structured as a maximum 80% combined loan-to-value across your existing mortgage and the bridge loan. On a $750K Sterling home with a $400K existing mortgage, you'd have roughly $200K of borrowing capacity through a bridge loan (80% of $750K = $600K total debt allowed, minus the $400K existing mortgage). Origination fees run 1.5–2%, and interest rates are typically 2–3 points above prime.

What are the Virginia transfer taxes when I sell my Sterling home?

Virginia charges a grantor's tax of $1 per $1,000 of sale price, paid by the seller. So on a $750K Sterling sale, the grantor tax is $750. Loudoun County (along with Fairfax, Arlington, Alexandria, Falls Church, and the City of Manassas) also applies a NOVA regional congestion tax of $0.15 per $100 of sale price — an additional $112 on $750K. Both are seller-paid at closing. There is no Virginia state real estate transfer tax beyond the grantor's tax.

How did the NAR settlement affect Sterling sell-and-buy transactions?

As of August 2024, buyer's agent commissions are no longer embedded in the listing commission and must be negotiated separately. For a Sterling sell-and-buy, this means two things: on your sell side, you negotiate the buyer agent compensation separately from the listing fee (most Sterling sellers still offer 2–2.5% to attract competitive buyer pools); on your buy side, you sign a buyer representation agreement specifying your agent's compensation, which can be paid by the seller, the buyer, or split.

What's the biggest mistake Sterling sellers make in a sell-and-buy?

The biggest mistake is shopping for the new home before listing the current one. Once you fall in love with a property in Ashburn, Brambleton, or Reston, you'll push a weak sale-contingent offer or feel forced to overprice your Sterling home to "make it work." The right sequence is: get your Sterling valuation, get pre-approved at both buy-first and sell-first scenarios, choose your strategy, prep and list — then engage seriously on the buy side once your Sterling home is on the market with a real list price.

Can I sell my Sterling home to The Jamil Brothers' cash offer program instead of going through a sell-and-buy?

Yes. For sellers whose situation calls for speed or certainty — a tight relocation timeline, an inherited Sterling property, a divorce, a home needing significant repairs, or simply preferring not to coordinate two open-market transactions — a cash offer eliminates the sell-side uncertainty entirely. Cash offers typically come in 5–15% below open-market value, so weigh that price haircut against the time, financing, and stress savings. We provide a side-by-side comparison of cash vs. open-market sale options at no obligation.

Glossary

Rent-Back (Post-Settlement Occupancy)

Contract addendum allowing the seller to stay in the home for an agreed number of days after closing in exchange for a daily fee paid to the new owner.

Bridge Loan

Short-term financing (6–12 months) secured by your current home, used to fund the down payment on a new home. Repaid when the current home sells.

HELOC

Home equity line of credit. A revolving credit line secured by your home's equity, typically with variable interest rates. Must be opened before listing the property.

Sale-Contingent Offer

An offer on a new home contingent upon the buyer's current home selling within a specified window. Rarely competitive in hot Northern Virginia markets.

Simultaneous Close

Both sell-side and buy-side closings occur on the same day, with sale proceeds wiring directly to fund the new home purchase.

Grantor's Tax

Virginia state transfer tax paid by the seller at $1 per $1,000 of sale price (0.1%).

NOVA Congestion Tax

Additional regional transfer tax ($0.15 per $100 of sale price) applied in Loudoun, Fairfax, Arlington, Alexandria, Falls Church, and Manassas. Paid by seller.

PITI

Principal, Interest, Taxes, and Insurance — the four core components of a total monthly mortgage payment. Used to calculate rent-back daily fees.

CMA

Comparative Market Analysis — a written report comparing your home to recently sold properties to establish a realistic list price.

Explore More

Browse Every Corner of the DMV Market

Whether you're searching by budget, neighborhood, or buying situation — find exactly what you need below.

Virginia Homes by Budget

Washington DC Homes by Budget

Maryland Homes

Explore Northern Virginia Communities

Loudoun County

Fairfax County & Surrounding

Ready to Make a Move?

Full-Service · No Tradeoffs

List for 1.5% & Keep More Equity

Professional photography, drone video, 3D tours, and expert negotiation — all included. On an $800K home, that's $12,000 more in your pocket vs. a 3% agent.

See the 1.5% Program →Need Speed or Certainty?

Get a No-Obligation Cash Offer

Skip the showings, skip the contingencies. If timing or condition matters more than top dollar, a cash offer may be the right fit. We'll walk you through every option.

Explore Cash Offers →

Categories

Recent Posts

Let's Connect