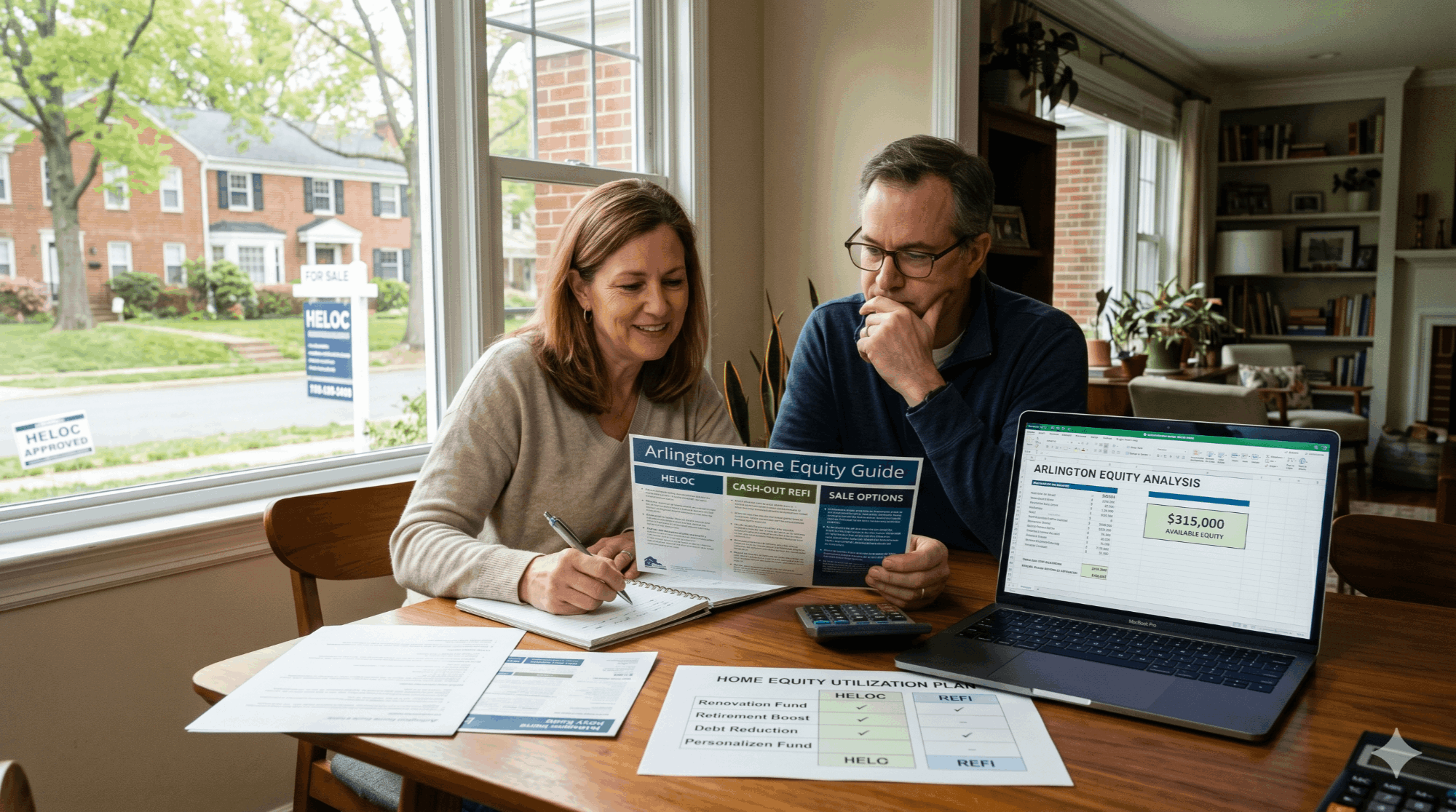

Home Equity in Arlington: HELOC, Cash-Out Refinance & Selling Options

Quick Answer: Arlington homeowners have three main ways to tap built-up home equity in 2026 — a Home Equity Line of Credit (HELOC), a cash-out refinance, or selling the home outright. HELOCs and cash-out refis let you stay in place but trade equity for new debt at today's higher interest rates, while selling — especially with a 1.5% full-service listing fee — unlocks 100% of your equity in cash and is often the highest-net option in a high-priced market like Arlington.

Arlington has been one of the strongest equity-builders in the entire DMV over the past decade. Pentagon-area condos, North Arlington single-family homes, and Ballston-Rosslyn corridor townhomes have all roughly doubled in value since the mid-2010s, while owners with sub-4% mortgages locked in during 2020-2021 are sitting on enormous unrealized gains. The decision in 2026 is no longer "do I have equity?" — it's "what's the smartest way to use it?"

This guide compares the three real options Arlington homeowners have — a HELOC, a cash-out refinance, and a strategic sale — with honest numbers, side-by-side cost breakdowns, and an Arlington-specific decision framework. We'll show what each path actually costs, who each one fits, and how a 1.5% full-service listing changes the math when selling is on the table.

Key Takeaways

- Most long-tenured Arlington owners have $300K–$700K+ in built equity — far more than they can responsibly access through a HELOC alone.

- HELOCs are flexible but variable-rate, currently averaging 8–9% APR in 2026; you only pay interest on what you draw.

- Cash-out refinances replace your existing mortgage at today's rates — costly if you locked in below 4% during 2020-2021.

- Selling unlocks 100% of equity tax-efficiently if you qualify for the IRS Section 121 primary-residence exclusion ($250K single / $500K married).

- On an $800K Arlington home, the difference between listing at 3% and listing at 1.5% full-service is roughly $12,000 — equity that stays with you, not the agent.

- The right choice depends on your interest rate, time horizon, life stage, and whether you'll actually use the equity productively.

In This Guide

- How much equity does the average Arlington homeowner have in 2026?

- Your Arlington Home Equity Options Compared

- Option 1: HELOC Options for Arlington Homeowners

- Option 2: Cash-Out Refinance Options in Arlington

- Option 3: Sell Your Arlington Home to Unlock Full Equity

- Arlington Home Equity Costs: HELOC vs. Refinance vs. Selling

- Arlington Home Sale Equity Calculator: 1.5% vs. 3% Listing Fee

- How Arlington Homeowners Should Choose Between a HELOC, Refinance or Selling

- Tax Implications of Accessing Home Equity in Arlington

- Arlington Real Estate Factors That Affect Home Equity Decisions

- Common Arlington Home Equity Mistakes to Avoid

- Why Arlington Homeowners Trust Us for Home Equity Guidance

- The Best Way to Access Home Equity in Arlington

- Arlington Home Equity FAQ

- Glossary

How much equity does the average Arlington homeowner have in 2026?

Arlington has had an unusual run. Median single-family home values across the county are now well above the $1M mark, and even modestly sized condos in Ballston, Clarendon, and Crystal City routinely close above $500K. Owners who bought before 2020 — particularly those who refinanced into the 2.5–3.5% rate window — are typically sitting on substantial paper equity.

The Federal Reserve's most recent Survey of Consumer Finances and quarterly homeowner equity reports from sources like ATTOM Data and CoreLogic have consistently shown the DC metro among the top markets nationally for percentage of "equity-rich" homeowners — defined as having mortgage balances of 50% or less of estimated property value. Arlington is well-represented inside that bucket.

~$1.05M

Median Arlington single-family value (estimated, early 2026)

~$580K

Median Arlington condo value (estimated, early 2026)

40%+

Share of Arlington owners considered "equity-rich"

If you bought a townhome in Courthouse for $625K in 2018 and it's worth roughly $850K today, with a balance of about $400K remaining, your accessible equity is in the $300K–$400K range depending on how much a lender will let you borrow against it. That's real money — and it's exactly the kind of position where the HELOC vs. refi vs. sell question becomes meaningful.

What is "tappable" equity vs. total equity?

Total equity is simply your home's market value minus what you owe. Tappable equity — the amount lenders will actually let you borrow against — is typically capped so that your total debt against the home stays at 80–85% of value. The remaining 15–20% has to stay as a buffer. So even with $400K in total equity, you may only be able to access $200K–$280K through a HELOC or refinance. Selling is the only path that unlocks 100% of your equity in one move.

Your Arlington Home Equity Options Compared

Each path has a different cost structure, a different timeline, and a different impact on your monthly cash flow. Before going deeper, here's the side-by-side.

| Factor | HELOC | Cash-Out Refi | Sell |

|---|---|---|---|

| How equity is unlocked | Revolving credit line | Lump sum at closing | Lump sum at sale |

| Typical max LTV | ~85% combined | ~80% | 100% (full sale) |

| Closing costs | $0–$3,000 (often waived) | 2–4% of new loan | Commission + transfer tax + fees |

| Interest rate (early 2026 ranges) | ~8–9% variable | ~6.5–7.25% fixed | N/A |

| Effect on existing mortgage | Untouched | Replaced | Paid off at closing |

| Adds new monthly payment? | Yes (after draw period) | Yes (replaces existing) | No |

| Best for | Short-term, flexible needs | Large lump-sum needs + better rate available | Major life change, downsizing, or maximizing equity |

Mortgage interest rate ranges above are illustrative based on early-2026 conditions and your actual quote will vary by credit, LTV, and lender. Always verify with two or three current lender quotes before deciding.

Option 1: HELOC Options for Arlington Homeowners

A HELOC is a revolving line of credit secured by your home. You're approved for a maximum amount — say $200,000 — and can draw against it as needed during a "draw period" (usually 10 years), paying interest only on the balance you actually use. After the draw period closes, you enter a repayment period (typically 10–20 years) where the balance amortizes like a normal loan.

When a HELOC makes sense for Arlington Homeowners

- You have a low-rate primary mortgage (sub-4%) you don't want to disturb.

- You need flexible access to funds — kitchen remodel paid in stages, college tuition over four years, a small investment property down payment.

- You're confident you'll pay it back relatively quickly, before the variable rate becomes painful.

- You only need a fraction of your tappable equity, not all of it.

The real costs and risks

HELOC rates in early 2026 are typically tied to the prime rate plus a margin, putting them in the 8–9% range. That's significantly higher than most existing first mortgages in Arlington, so HELOCs really shine when used as short-term capital, not as a long-term financing tool. The rate also moves — if the Fed shifts, your payment shifts. And because the loan is secured by your home, a missed payment can ultimately threaten the property itself.

| Pros | Cons |

|---|---|

| Doesn't disturb low-rate first mortgage | Variable rate — payments can climb |

| Pay interest only on what you draw | Capped at ~85% combined LTV |

| Closing costs often waived or minimal | Lender can freeze the line if values drop |

| Flexible draw and repayment | Adds a second payment after draw period |

Before you pick HELOC, refi, or sell — anchor the conversation in real numbers. Get a personalized Arlington valuation from The Jamil Brothers using street-level comps, not automated estimates. Response within 24 hours.

Option 2: Cash-Out Refinance Options in Arlington

A cash-out refinance replaces your existing mortgage with a new, larger one — and you pocket the difference. If you owe $400K on a home worth $850K and refinance into a new $600K loan, you walk away with roughly $200K in cash (minus closing costs) and a brand-new monthly payment.

When Arlington Homeowners Should Consider a Cash-Out Refinance

- Your existing mortgage rate is similar to or higher than today's rates — so you're not giving up much.

- You need a large, defined lump sum (debt consolidation, major home addition, or business capital).

- You want a fixed payment for predictability rather than a variable HELOC.

- You plan to stay in the home long enough to recoup the closing costs, typically 5+ years.

The catch most Arlington homeowners face

The single biggest reason a cash-out refi often doesn't make sense in Arlington in 2026 is what's called the "lock-in effect." Owners who refinanced during the 2020-2021 rate trough are sitting on mortgages at 2.75%, 3.0%, or 3.25%. Replacing that loan with a new mortgage at 6.5–7.25% means dramatically higher monthly payments — even before you touch a dollar of cash-out. For many owners, the math only works if they urgently need the cash and have no other access.

⚠️ The Lock-In Trap

If your current mortgage is below 4%, a cash-out refi can easily double your monthly interest expense on the same balance. Run the numbers carefully — sometimes a HELOC for short-term needs, or a sale for major life changes, beats giving up a once-in-a-generation mortgage rate.

| Pros | Cons |

|---|---|

| Single fixed-rate payment | Replaces low-rate mortgage at today's rates |

| Larger lump sum than a HELOC | 2–4% closing costs on the new loan |

| Predictable amortization schedule | Resets your loan clock to 30 years |

| Interest may be deductible if used for home improvements | Capped at ~80% LTV — leaves equity stranded |

Option 3: Sell Your Arlington Home to Unlock Full Equity

Selling is the only path that actually puts your full equity to work. There's no LTV cap, no new monthly payment, no variable-rate exposure. You walk away from closing with a check (or wire) representing the sale price, minus your remaining mortgage payoff, minus closing costs and commission.

For Arlington owners experiencing a major life change — empty-nesting, downsizing to a condo, relocating for a federal or contractor job, retirement, or moving closer to family — selling typically delivers the highest net dollar amount of the three options. And because most primary-residence sellers qualify for the IRS Section 121 capital gains exclusion ($250K for single filers, $500K for married couples filing jointly), much of the gain may come out tax-free.

Why listing fees matter when accessing home in equity in Arlington

Commission is the single biggest controllable cost in a home sale. On an $850K Arlington sale, a traditional 3% listing fee equals $25,500 — enough to fully fund a new car, a year of college, or a sizable down payment on a downsize. Cutting that fee in half through a 1.5% full-service program puts $12,750 back in your pocket without giving up professional photography, drone video, 3D tours, or expert negotiation.

That's the foundation of our 1.5% full-service listing program — full marketing, full negotiation, full MLS exposure, at half the typical listing fee. The savings are real and they go directly to the seller's net.

What's included in The Jamil Brothers' 1.5% full-service program

- Professional 4K photography and drone video

- 3D Matterport virtual tour

- Full MLS exposure across BrightMLS plus syndication to Zillow, Realtor.com, Redfin, and Homes.com

- Custom Arlington-area marketing strategy with neighborhood-specific positioning

- Pricing analysis using street-level comps, not algorithms

- Expert offer review and contract negotiation by a partner-level broker

- Coordination of inspections, appraisal, and final walk-through

- Closing oversight start to finish

Arlington Home Equity Costs: HELOC vs. Refinance vs. Selling

Below is a typical cost picture for an Arlington homeowner with an $850,000 home, a $400,000 remaining mortgage balance at 3.25%, and a need to access roughly $200,000 in equity. The exact numbers will vary by lender, credit profile, and current market conditions, but the relative differences hold.

| Cost or impact | HELOC ($200K line) | Cash-Out Refi (new $600K loan) | Sale (full $850K) |

|---|---|---|---|

| Upfront fees | $0–$2,000 | ~$15,000–$22,000 (2.5–3.5%) | Commission + transfer + closing fees |

| Listing commission cost | $0 | $0 | $12,750 at 1.5% / $25,500 at 3% |

| VA grantor tax (~$1/$1,000) | $0 | $0 | ~$850 |

| NOVA congestion fee (0.15%) | $0 | $0 | ~$1,275 |

| New monthly P&I | ~$1,500 if fully drawn at 8.5% | ~$3,950 at 6.875% | $0 — mortgage extinguished |

| Cash you actually receive | Up to $200K (drawn over time) | ~$180K–$185K after fees | ~$405K–$420K (1.5%) / ~$390K–$405K (3%) |

Two things jump out: first, a sale unlocks roughly twice as much net cash as a HELOC or cash-out refi in this scenario. Second, on the sale side alone, the difference between listing at 1.5% versus 3% is roughly $12,000–$13,000 of additional equity in the seller's pocket.

How much Arlington home equity each option unlocks

Net cash to seller, $850K Arlington home, $400K mortgage payoff. Closing costs estimated at 1% of sale price. Buyer agent compensation negotiable post-NAR settlement.

Arlington Home Sale Equity Calculator: 1.5% vs. 3% Listing Fee

If a sale is on the table, the listing fee is the single biggest line item you can control. Use the calculator below to see your net proceeds at five Arlington-relevant price points, comparing a traditional 3% agent against The Jamil Brothers' 1.5% full-service listing program.

arlington Seller Savings Calculator

How much more do you keep with our 1.5% listing fee?

Select your Arlington home's estimated value to see your real net proceeds — side by side.

Traditional Agent — 3%

| Sale price | $400,000 |

| Listing fee (3%) | −$12,000 |

| Buyer's agent (2.5%) | −$10,000 |

| Est. closing (1%) | −$4,000 |

| Net Proceeds | $374,000 |

Our Fee — Only 1.5%

| Sale price | $400,000 |

| Listing fee (1.5%) | −$6,000 |

| Buyer's agent (2.5%) | −$10,000 |

| Est. closing (1%) | −$4,000 |

| Net Proceeds | $380,000 |

Extra in your pocket

$6,000

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

| Sale price | $500,000 |

| Listing fee (3%) | −$15,000 |

| Buyer's agent (2.5%) | −$12,500 |

| Est. closing (1%) | −$5,000 |

| Net Proceeds | $467,500 |

Our Fee — Only 1.5%

| Sale price | $500,000 |

| Listing fee (1.5%) | −$7,500 |

| Buyer's agent (2.5%) | −$12,500 |

| Est. closing (1%) | −$5,000 |

| Net Proceeds | $475,000 |

Extra in your pocket

$7,500

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

| Sale price | $600,000 |

| Listing fee (3%) | −$18,000 |

| Buyer's agent (2.5%) | −$15,000 |

| Est. closing (1%) | −$6,000 |

| Net Proceeds | $561,000 |

Our Fee — Only 1.5%

| Sale price | $600,000 |

| Listing fee (1.5%) | −$9,000 |

| Buyer's agent (2.5%) | −$15,000 |

| Est. closing (1%) | −$6,000 |

| Net Proceeds | $570,000 |

Extra in your pocket

$9,000

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

| Sale price | $750,000 |

| Listing fee (3%) | −$22,500 |

| Buyer's agent (2.5%) | −$18,750 |

| Est. closing (1%) | −$7,500 |

| Net Proceeds | $701,250 |

Our Fee — Only 1.5%

| Sale price | $750,000 |

| Listing fee (1.5%) | −$11,250 |

| Buyer's agent (2.5%) | −$18,750 |

| Est. closing (1%) | −$7,500 |

| Net Proceeds | $712,500 |

Extra in your pocket

$11,250

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

| Sale price | $1,000,000 |

| Listing fee (3%) | −$30,000 |

| Buyer's agent (2.5%) | −$25,000 |

| Est. closing (1%) | −$10,000 |

| Net Proceeds | $935,000 |

Our Fee — Only 1.5%

| Sale price | $1,000,000 |

| Listing fee (1.5%) | −$15,000 |

| Buyer's agent (2.5%) | −$25,000 |

| Est. closing (1%) | −$10,000 |

| Net Proceeds | $950,000 |

Extra in your pocket

$15,000

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Estimates only. Closing costs vary. Buyer's agent commission is negotiable post-NAR settlement.

4K photography, drone video, 3D tours, expert negotiation, and full MLS marketing — all included at 1.5%. No hidden fees, no service reductions, no surprises.

How Arlington Homeowners Should Choose Between a HELOC, Refinance or Selling

The right answer depends on four variables: how much equity you actually need, your existing mortgage rate, your time horizon in the home, and your tolerance for new debt. Walk through these four questions in order.

How much do you actually need — and for what?

If it's a $40K kitchen remodel paid in stages, a HELOC fits cleanly. If it's $250K to fund a child's college plus a major addition, a refi or sale may be required. If it's "I want to use my equity to buy something better suited to my next stage of life," you're describing a sale.

What's your current mortgage rate?

If you're under 4%, protect that loan. Use a HELOC (which leaves it intact) or sell (which extinguishes it but trades for cash). A cash-out refi typically destroys more value than it creates when your existing rate is well below market.

How long do you plan to stay?

If you're moving in the next 2–3 years anyway, paying $15K–$22K in cash-out refi fees rarely pencils out. Either bridge the gap with a HELOC or move the timeline up and sell.

Are you trying to stay or trying to leave?

If you genuinely love the home and want to age in place or stay long-term, HELOC or refi keeps you in. If the home no longer fits your stage of life — too big, too much yard, wrong school district, no longer near work — selling is almost always the better outcome financially and personally.

Quick Arlington Home Equity Decision Checklist

Sell if more than three apply

- The home no longer fits your size, stage, or location needs

- You're paying more than $1,500/month in upkeep, taxes, and insurance combined

- You'd downsize anyway in the next 3–5 years

- You want to fully eliminate mortgage debt

- You qualify for the IRS Section 121 capital gains exclusion

- You'd reinvest the proceeds (next home, retirement accounts, business)

- Selling activity in your Arlington micro-market is healthy with reasonable days on market

Tax Implications of Accessing Home Equity in Arlington

Each option has a different tax footprint. None of this is tax advice — confirm your specific situation with a CPA — but the broad strokes matter when you're comparing.

| Option | Federal tax treatment | Common pitfalls |

|---|---|---|

| HELOC | Interest deductible only if used for substantial home improvements (post-2017 TCJA rules); not deductible for general consumer use. | People assume HELOC interest is always deductible — it isn't. |

| Cash-Out Refi | Interest on the original mortgage portion remains deductible. Interest on the cash-out portion follows the same home-improvement rule. | The "acquisition debt" portion gets refreshed only up to your prior balance. |

| Sale | Section 121 exclusion: $250K (single) / $500K (married filing jointly) of gain excluded if home was primary residence for 2 of past 5 years. Excess gain is long-term capital gain. | Investment properties or homes you've rented don't qualify; holding period rules are strict. |

ℹ️ Section 121 in real Arlington numbers

If a married couple bought a Lyon Park home for $475K in 2010 and sells in 2026 for $1.1M, their gross gain is roughly $625K. The first $500K is excluded under Section 121 — so only $125K is taxed as long-term capital gain, before any further adjustments for selling costs and capital improvements documented over the years.

Arlington Real Estate Factors That Affect Home Equity Decisions

Arlington isn't a generic market and three local realities reshape the equity decision.

How Federal Employment Impacts Arlington Home Equity Decisions

A large share of Arlington owners work for the federal government, large contractors, or Pentagon-adjacent agencies. PCS orders, contract endings, agency reorganizations, and reductions in force can all force a sudden timeline. If there's any chance you'll need to relocate within 24 months, locking yourself into a new 30-year cash-out refi is rarely the right move — a HELOC is more flexible, and selling on your own timeline is even better.

Arlington Condo vs. Single-Family Home Equity Trends

Arlington has two distinct equity stories. North Arlington single-family homes have appreciated steadily and predictably; equity unlocks usually proceed without surprises. Condos, particularly in Ballston, Crystal City, and Pentagon City, have more variable performance — newer luxury buildings, special assessments, and rental-cap rules in some HOAs can affect what a lender lets you borrow against and what a buyer is willing to pay. If you own a condo, get a current valuation before assuming your tappable equity number.

Understanding The Section 121 Tax Exclusion for Arlington Sellers

Long-tenured Arlington owners often have appreciation that pushes right up against — or beyond — the $500K married-couple Section 121 cap. Selling earlier rather than later, while the gain still fits inside the exclusion, can be more tax-efficient than waiting another five years and crossing the threshold. This is a real planning question that an Arlington-experienced agent paired with a CPA can map out.

Our seller net sheet calculator breaks down every cost — Virginia grantor tax, NOVA congestion fee, commission, closing fees — so you know your real bottom line before deciding between HELOC, refi, or sale.

Common Arlington Home Equity Mistakes to Avoid

⚠️ Mistake #1 — Treating equity like spending money

Equity is built capital, not income. Using a HELOC or cash-out refi to fund vacations, vehicles, or short-term lifestyle upgrades converts long-term wealth into long-term debt at high rates. Reserve equity moves for productive uses: home improvements that hold value, education, business capital, or right-sizing your housing.

⚠️ Mistake #2 — Refinancing out of a sub-4% mortgage

The lock-in math is brutal. Replacing a 3.0% mortgage with a 6.875% one on the same balance can roughly double your monthly interest expense — before the cash-out portion even shows up. Run the numbers explicitly before any cash-out refi conversation goes further.

⚠️ Mistake #3 — Skipping a current-market valuation

Estimating tappable equity from Zillow or a 2022 appraisal leads to wildly off planning numbers. Arlington micro-markets shift; condo values especially can vary by building. Get a 2026 valuation before you start applying for anything.

⚠️ Mistake #4 — Choosing the listing agent based on the first conversation

If you decide to sell, the listing agent decision is the largest financial decision inside the sale. Interview at least two. Ask each one for: their actual recent Arlington comparable sales, their fee structure, what marketing is included, and how they handle multiple-offer negotiation. The cheapest fee with weak service costs you more than a fair fee with full service.

How to choose the right listing agent in Arlington

Strong Arlington listing agents share four traits regardless of fee structure: they have actual recent sales in your specific Arlington micro-market, they bring a written marketing plan rather than improvising, they negotiate from data rather than hope, and they're transparent about every line item in the closing statement.

The Jamil Brothers Realty Group has closed over 840 homes across Northern Virginia, holds NVAR Lifetime Top Producer status, and runs a 1.5% full-service listing program for Arlington sellers — full marketing and full negotiation, with the saved commission staying in your equity.

If timing, condition, or certainty matters more than maximum price — for example, an inherited Arlington home, a divorce settlement, or a fast PCS — a cash offer may be the right fit. We'll walk you through your full range of options, no pressure.

Why Arlington Homeowners Trust Us for Home Equity Guidance

Arlington homeowners trust The Jamil Brothers Realty Group for local market expertise, pricing strategy, and full-service support. We help homeowners compare HELOCs, cash-out refinancing, and selling options using real Arlington market data instead of automated estimates.

Our Experience Helping Arlington Homeowners Unlock Home Equity

We've helped Arlington homeowners:

- Unlock equity through strategic home sales

- Evaluate HELOC and refinance options against current market conditions

- Downsize while maximizing net proceeds at closing

- Navigate relocation and timing decisions with confidence

Our focus is helping sellers keep more of their equity while making informed financial decisions.

Recent Arlington Home Equity Success Stories

From North Arlington single-family homes to Ballston condos, we've helped homeowners compare selling, refinancing, and HELOC strategies based on mortgage rates, equity position, market timing, and long-term financial goals. Every Arlington property and homeowner situation requires a different approach — and our role is to map your specific numbers against your specific goals before any decision is made.

How We Analyze Arlington Home Equity and Home Values Beyond Zillow

Our valuation process includes:

- Recent Arlington comparable sales pulled from BrightMLS, not algorithms

- Current market inventory trends by neighborhood and property type

- Condo and HOA financial analysis for Ballston, Crystal City, and Pentagon City units

- Buyer demand patterns specific to your micro-market

- Realistic seller net proceeds estimates including all Virginia closing costs

This helps homeowners make better home equity decisions using accurate local market data — not generic national averages.

Meet the Arlington Home Equity and Real Estate Experts Behind This Guide

This guide was created by The Jamil Brothers Realty Group, a Northern Virginia real estate team led by Saad Jamil and Arslan Jamil — licensed Associate Brokers with Samson Properties specializing in Arlington home sales, equity planning, pricing strategy, and seller representation. With 840+ homes sold, $500M+ in closed volume, and NVAR Lifetime Top Producer status, our goal is to help homeowners understand the real financial impact of HELOCs, refinancing, and selling.

Sources Behind Our Arlington Home Equity Market Analysis

This guide references:

- BrightMLS housing trends and recent Arlington comparable sales

- Federal Reserve homeowner equity data and Survey of Consumer Finances

- IRS Section 121 capital gains exclusion guidance

- Virginia seller closing cost structures (grantor tax, NOVA congestion fee)

- Arlington market activity and pricing trends from local MLS data

Market conditions and lending standards can change, so homeowners should always verify financial and tax decisions with licensed professionals before acting.

Updated for 2026 Arlington Home Equity and Housing Market Trends

This guide reflects 2026 Arlington market conditions, including HELOC rate trends, cash-out refinance conditions, home appreciation, seller costs, and post-NAR settlement commission updates. Homeowners should review updated market data and lender quotes before making major equity decisions — and we're happy to walk through your specific Arlington numbers at no cost.

Explore More Northern Virginia Guides

Alexandria McLean Vienna Fairfax Reston Ashburn 1.5% Listing Program Seller Net Sheet Cash Offers Search HomesKnow your Arlington home's current value, understand your costs, and see exactly what you'd walk away with at sale — before you commit to a HELOC, refi, or listing. The Jamil Brothers provide a full seller consultation at no cost or obligation.

The Best Way to Access Home Equity in Arlington Depends on Your Goals

HELOC, cash-out refinance, and sale all unlock equity — but they unlock different amounts, at different costs, with different long-term consequences. For owners with sub-4% mortgages who only need short-term flexibility, a HELOC almost always wins. For owners who need a large lump sum and have rates near or above current market, a cash-out refi can pencil out. For owners whose homes no longer fit their lives, or who want to convert built equity into cash with no new monthly payment, selling — especially through a 1.5% full-service listing program — typically delivers the highest net dollar amount and the cleanest financial reset.

The right answer is specific to your numbers. Anchor it in real Arlington comparable sales, verified mortgage quotes, and a CPA's read on your tax position. The goal isn't to pick a path on principle — it's to pick the path that puts the most net equity to work for the next stage of your life.

Arlington Home Equity FAQ

What's the difference between a HELOC and a home equity loan?

A HELOC is a revolving line of credit — you can draw, repay, and redraw during the draw period, paying interest only on the balance you actually use. A home equity loan (sometimes called a second mortgage) is a fixed lump sum at a fixed rate, repaid on a set schedule. HELOCs offer flexibility; home equity loans offer payment predictability. Both are secured by your Arlington home and both leave your existing first mortgage untouched.

How much equity can I borrow against my Arlington home?

Most Arlington lenders cap combined loan-to-value (CLTV) at 80–85% of current appraised value. So on an $850,000 Arlington home with a $400,000 first mortgage balance, your tappable equity is roughly $280,000–$320,000 depending on the specific lender and your credit profile. This is total borrowing capacity across both your existing mortgage and any new HELOC or second loan combined.

Should I do a cash-out refinance if my mortgage rate is below 4%?

Almost never. Replacing a sub-4% mortgage with a current 6.5–7.25% loan dramatically increases your monthly interest expense even on the same balance. For most Arlington owners with 2020-2021 era loans, a HELOC is far better for short-term capital needs, and a sale makes more sense than a refi for major life-stage transitions. Run the numbers explicitly before considering a cash-out refi when you have a low-rate first mortgage.

How long does it take to close a HELOC vs. a cash-out refinance vs. a home sale?

HELOCs typically close in 3–5 weeks from application to funding in Arlington. Cash-out refinances usually take 30–45 days, similar to a purchase mortgage. A home sale, when properly listed and priced, usually takes 30–60 days from listing to closing in current Arlington market conditions, though specific timelines depend on price point, condition, and demand for your property type.

Is interest on a HELOC tax-deductible in 2026?

Only if the funds are used for substantial home improvements on the property securing the loan. Under post-2017 Tax Cuts and Jobs Act rules, HELOC interest used for general consumer purposes — paying off credit cards, buying a car, taking a vacation — is not deductible. If you're using the HELOC to renovate your Arlington home, document the use carefully and consult a CPA. Tax laws can change, so verify before relying on any deduction.

How does the Section 121 capital gains exclusion work for Arlington sellers?

If you've owned and lived in your Arlington home as your primary residence for at least 2 of the past 5 years, you can exclude up to $250,000 of capital gain (single filers) or $500,000 (married filing jointly) from federal taxes when you sell. Long-tenured Arlington owners often see appreciation that comes close to or exceeds these limits, which is why timing of a sale can have meaningful tax consequences. Confirm your specific situation with a CPA familiar with Virginia and federal residential rules.

What are the typical closing costs when selling in Arlington?

Arlington sellers typically pay listing commission (1.5% with The Jamil Brothers' full-service program, traditionally 3% elsewhere), Virginia grantor's tax of about $1 per $1,000 of sale price, the Northern Virginia Congestion Relief Fee of 0.15% of sale price, settlement and recording fees, and any HOA or condo association transfer fees if applicable. On an $850,000 sale, total seller closing costs (excluding commission) typically run $5,000–$9,000.

How did the NAR settlement change buyer's agent commission for Arlington sellers?

As of August 2024, buyer's agent compensation is no longer required to be advertised on the MLS or pre-set by the listing agreement. Sellers can choose whether and how much to offer toward the buyer's representation, and buyer's agents must have written compensation agreements directly with their clients. In practice, most Arlington sellers still offer some buyer-agent compensation (typically 2–2.5%) to maximize buyer pool reach, but the rate is fully negotiable on every transaction.

Does the HOA at my Arlington condo affect how much equity I can tap?

It can. Lenders evaluate the financial health of the condo association, the percentage of owner-occupied units, any pending special assessments, and rental restrictions. If the HOA has weak reserves or large pending assessments, lenders may reduce the maximum loan-to-value they'll allow on a HELOC or refi against your unit. The same factors affect a sale — buyers and their lenders look at the same association documents.

Is the Arlington market still favorable for sellers in 2026?

Arlington remains a relatively tight market in 2026. The combination of federal employment stability, Amazon HQ2 hiring momentum, Metro access, and limited new construction continues to support pricing in well-prepared homes that are priced to current comparable sales. Days on market and price-to-list ratios vary by neighborhood and property type, so a current-market valuation is essential before assuming your specific home will sell quickly. Verify current trends with up-to-date BrightMLS data or a local Arlington agent.

Can I tap equity through a HELOC and then sell soon after?

Yes, but the HELOC balance gets paid off at closing from sale proceeds, just like the first mortgage. If you draw $100,000 on a HELOC and then sell six months later, that $100,000 plus any interest accrued comes off your net proceeds at settlement. Some lenders also charge early-closure fees if a HELOC is paid off and closed within the first three years, so check your specific HELOC terms before drawing.

How do I choose between The Jamil Brothers' 1.5% program and a traditional 3% Arlington listing agent?

Compare three things: included services, agent track record, and total cost to you. The Jamil Brothers' 1.5% program includes professional photography, drone video, 3D Matterport tours, full MLS marketing, expert negotiation by an Associate Broker, and complete transaction management — the same scope of work many traditional 3% agents provide. With over 840 homes sold and NVAR Lifetime Top Producer status, the 1.5% structure simply means more of your equity stays with you at closing rather than being paid to a higher commission. Always interview at least two agents and ask for a written marketing plan before signing anything.

Glossary

HELOC

Home Equity Line of Credit — a revolving credit line secured by your home, with a variable rate, a draw period (usually 10 years) and a repayment period (usually 10–20 years).

Cash-Out Refinance

A refinance that replaces your existing mortgage with a larger one, paying you the difference in cash at closing minus loan costs.

LTV / CLTV

Loan-to-Value / Combined Loan-to-Value — the ratio of total loan balance(s) to the home's appraised value. Most home-equity products cap CLTV at 80–85%.

Section 121 Exclusion

The federal tax provision allowing a primary residence seller to exclude up to $250K (single) or $500K (married filing jointly) of capital gain from federal income tax, subject to ownership and use tests.

Lock-In Effect

The reluctance to refinance or sell because your existing mortgage rate is far below current market rates, making any new mortgage substantially more expensive on the same balance.

NOVA Congestion Relief Fee

A 0.15% transfer tax applied at closing in Northern Virginia jurisdictions (including Arlington), in addition to the state grantor's tax. Paid by the seller.

Grantor's Tax

Virginia's state-level transfer tax on real estate sales, calculated at approximately $1 per $1,000 of sale price, paid by the seller at closing.

Tappable Equity

The portion of your home equity you can actually borrow against — total equity minus the lender's required cushion (typically the top 15–20% of the home's value).

Explore More

Browse Every Corner of the DMV Market

Whether you're searching by budget, neighborhood, or buying situation — find exactly what you need below.

Virginia Homes by Budget

Washington DC Homes by Budget

Maryland Homes

Explore Northern Virginia Communities

Loudoun County

Fairfax County & Surrounding

Ready to Make a Move?

Full-Service · No Tradeoffs

List for 1.5% & Keep More Equity

Professional photography, drone video, 3D tours, and expert negotiation — all included. On an $800K home, that's $12,000 more in your pocket vs. a 3% agent.

See the 1.5% Program →Need Speed or Certainty?

Get a No-Obligation Cash Offer

Skip the showings, skip the contingencies. If timing or condition matters more than top dollar, a cash offer may be the right fit. We'll walk you through every option.

Explore Cash Offers →Categories

Recent Posts

Let's Connect