Tapping Into Home Equity in McLean: HELOC, Cash-Out Refi & Sale Options

Tapping Into Home Equity in McLean: HELOC, Cash-Out Refi & Sale Options

Quick Answer: McLean homeowners have three primary ways to access equity: a HELOC (flexible credit line at variable rates), a cash-out refinance (one new fixed-rate mortgage that replaces the existing one), or selling the home outright. HELOCs and cash-out refis preserve your home but add debt; selling unlocks 100% of your equity but ends ownership. With McLean's median home value above $1.5M, the math on each option carries six-figure stakes — making the listing fee on a sale (3% vs. 1.5%) often the single largest variable in your final cash position.

Key Takeaways

- Most McLean homeowners hold $500K–$1.2M+ in equity due to long-term appreciation in 22101 and 22102.

- A HELOC works best for short-term, flexible draws (renovations, education, bridge funds) — variable rate, low closing costs.

- A cash-out refinance works best when you want a large lump sum at a fixed rate and plan to keep the home long-term.

- Selling is the only option that converts 100% of your equity to cash — but your listing commission directly determines how much you keep.

- On a $1.5M McLean sale, the difference between a 3% and a 1.5% listing fee is $22,500 — equivalent to a year of property taxes plus a luxury vacation.

- Federal tax law (TCJA) limits HELOC and cash-out interest deduction to funds used to "buy, build, or substantially improve" the home — non-improvement use loses the deduction.

In This Guide

- McLean Home Equity Snapshot 2026

- The Three Ways to Access Your Equity

- Option 1: HELOC (Home Equity Line of Credit)

- Option 2: Cash-Out Refinance

- Option 3: Selling Your McLean Home

- Side-by-Side Comparison

- Tax Implications of Each Option

- How to Choose the Right Option

- McLean Market in 2026 — Impact on Each Option

- The Hidden Cost of Selling: Why 1.5% Matters

- Common Equity Mistakes McLean Homeowners Make

- Frequently Asked Questions

- Glossary

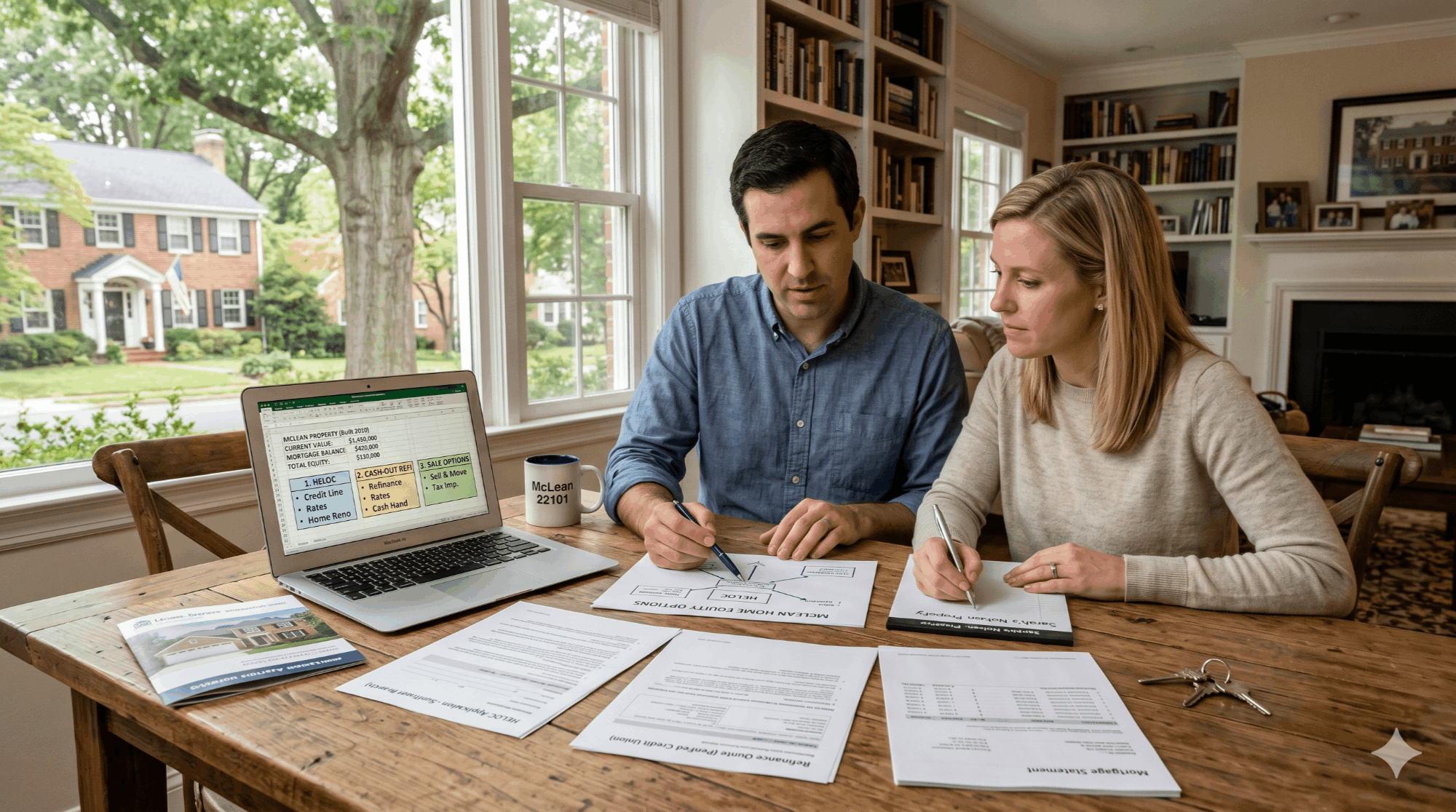

If you've owned a home in McLean for more than five years, you are almost certainly sitting on substantial equity. Years of price appreciation along the Dulles Corridor — combined with the McLean ZIP codes' enduring demand from federal contractors, finance professionals, and CIA-adjacent employers — have pushed median values past $1.5 million in many sub-neighborhoods. For homeowners considering renovations, college costs, debt consolidation, retirement repositioning, or simply lifestyle change, that equity is no longer a passive number on a Zillow page. It's a real, accessible asset.

The question is no longer whether you have equity. It's which path makes the most sense for converting it into cash, freedom, or a different kind of asset altogether. The three primary tools are a Home Equity Line of Credit (HELOC), a cash-out refinance, and an outright sale. Each comes with its own cost structure, timeline, tax treatment, and risk profile — and in a market like McLean, where the dollars at stake are larger than most national averages, choosing the wrong tool can quietly cost you tens of thousands.

This guide breaks down all three, side by side, with the local context that matters: McLean-specific home values, real Northern Virginia closing costs, the post-NAR settlement commission landscape, and the ways that even small percentage differences (like 3% vs. 1.5% listing fees) translate into life-changing dollars on a $1.5M sale.

McLean Home Equity Snapshot 2026

McLean's residential market spans two primary ZIP codes — 22101 (central McLean, including downtown, Salona Village, Chesterbrook) and 22102 (Tysons-adjacent, including parts of Pimmit Hills and the Falls Church/McLean border) — plus pockets that touch 22043 and 22066. Long-term appreciation has been robust, and most owners holding properties for 7+ years have crossed into the "high-equity" zone where conventional 80% loan-to-value lending unlocks meaningful capital.

| McLean Equity Profile (Typical Ranges) | 5-Year Owners | 10-Year Owners | 15+ Year Owners |

|---|---|---|---|

| Estimated current value | $1.2M–$1.6M | $1.5M–$2.0M | $1.7M–$2.5M+ |

| Typical remaining mortgage | $700K–$1.0M | $400K–$700K | $0–$400K |

| Approximate equity | $300K–$700K | $800K–$1.4M | $1.4M–$2.5M |

| Max accessible at 80% LTV | $260K–$500K | $700K–$1.1M | $1.1M–$1.6M |

Ranges are illustrative based on McLean (22101/22102) market patterns. Actual values depend on lot size, school pyramid (McLean HS vs. Langley HS), renovation history, and proximity to Tysons/I-495. For a current value, see your McLean home market overview.

How to Calculate Your Own McLean Equity Position

The formula is simple. Your equity is your home's current market value, minus your remaining mortgage balance, minus any other liens (HELOC, second mortgage, judgment). What's tricky is the "current market value" piece — Zestimate-style automated valuations frequently mis-price McLean homes by $100K or more in either direction, because the market has wide pricing variance based on lot, finish level, and which side of Old Dominion Drive you're on. A street-level comparative market analysis (CMA) from a local agent is the only reliable way to know your real number.

Skip the algorithmic estimates. Get a street-level market analysis from The Jamil Brothers — comps from your specific McLean sub-neighborhood, adjustment for finish level and lot, and a real number you can plan around. Response within 24 hours.

The Three Ways to Access Your Equity

Before drilling into each option, here's the high-level framing every McLean homeowner should understand. The three tools are not equivalent — they exist on a spectrum from "borrow against your equity while keeping the home" to "convert your equity entirely to cash by leaving."

| Path | What It Does | Equity Released | Keep the Home? |

|---|---|---|---|

| HELOC | Variable-rate credit line, draw as needed | Up to ~80% LTV minus existing mortgage | Yes |

| Cash-Out Refi | Replaces existing mortgage; fixed-rate lump sum | Up to ~80% LTV minus existing mortgage | Yes |

| Sale | Liquidates the asset entirely | 100% of equity (after costs) | No |

Critically, the first two options (HELOC and cash-out refi) only let you access roughly 80% of your home's value minus what you already owe. So if your McLean home is worth $1.5M and you owe $500K on the existing mortgage, your maximum borrow is $1.2M − $500K = $700K. A sale, by contrast, gives you access to the full equity (after commission and closing costs).

Option 1: HELOC (Home Equity Line of Credit)

A HELOC is a revolving credit line secured by your home — think of it as a credit card with your house as collateral. You're approved for a maximum amount, and you can draw against it during a "draw period" (typically 10 years) and repay during a "repayment period" (typically 10–20 years). You pay interest only on what you've actually drawn, not the full credit line.

How a HELOC Works in Practice

You apply with a bank or credit union (Pentagon Federal, Navy Federal, Apple FCU, and Sandy Spring Bank are popular Northern Virginia HELOC providers). The lender orders an appraisal, pulls your credit, verifies income, and approves a credit line typically capped at 80% combined loan-to-value (CLTV). So if your McLean home appraises at $1.5M and you owe $500K on the first mortgage, your HELOC could be sized up to $1.2M − $500K = $700K.

Most HELOCs are variable rate, indexed to the Wall Street Journal Prime Rate plus a margin (typically 0% to 2%). When the Federal Reserve moves rates, your HELOC rate moves with it — usually within one billing cycle. This is the single biggest risk of a HELOC: payments can rise quickly in a rising-rate environment.

HELOC Cost Breakdown — McLean Borrower Example

- Application/origination fees: $0–$500 (often waived)

- Appraisal: $500–$800 (sometimes lender-paid)

- Title search and recording fees: $200–$500

- Annual fee (some lenders): $50–$100

- Total upfront: typically $500–$1,500 (vs. tens of thousands for a refi)

- Interest rate: Prime + 0.5% to 2% (variable)

HELOC Pros and Cons

| ✓ Pros | ✗ Cons |

|---|---|

| Low/no closing costs — fast approval (2–4 weeks) | Variable rate — payments can rise unexpectedly |

| Pay interest only on what you draw, not the line | Doesn't replace your existing mortgage's rate |

| Flexible draws over 10 years — useful for renovations | Lender can freeze/reduce the line if values drop |

| Preserves your existing low mortgage rate (if you have one) | Discipline required — easy to over-draw |

When a HELOC Makes Sense in McLean

HELOCs shine when you need flexible, short-to-medium-term capital — and especially when your existing first mortgage rate is below current refinance rates. If you locked in a 3% mortgage in 2020 or 2021, a cash-out refi at today's rates would force you to give up that low rate on your entire balance. A HELOC keeps the existing first mortgage untouched and only carries a higher rate on the additional borrowing. Common McLean use cases include kitchen/bath renovations, college tuition for one or two years, bridge financing while waiting for a property sale, or a hedge against unexpected expenses.

Option 2: Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a new, larger one — and you pocket the difference at closing as a tax-free lump sum (technically, loan proceeds aren't income, so they aren't taxed). Unlike a HELOC, this is a full mortgage transaction: new application, new appraisal, new title work, new closing.

How a Cash-Out Refi Works in Practice

Say your McLean home appraises at $1.5M, and your existing mortgage balance is $500K. A cash-out refi at 80% LTV would create a new $1.2M mortgage. You use $500K of that to pay off the old loan, plus $20K–$30K in closing costs, and walk away with roughly $670K–$680K in cash. Your monthly payment will be larger (because the loan is larger), but it's fixed for the life of the new loan — typically 15 or 30 years.

Cash-Out Refi Closing Cost Profile (Relative to HELOC)

All ranges based on a $1.5M McLean home. Sale figures include commission plus standard Virginia closing costs (grantor tax, NOVA congestion tax, settlement fees, HOA transfer where applicable).

Cash-Out Refi: When It's the Right Move

Cash-out refinances make the most sense when (1) current rates are at or below your existing mortgage rate, so you're not "trading up" to a worse rate; (2) you want a large lump sum at a fixed payment for predictable budgeting; (3) you plan to keep the home for at least 5–7 more years to amortize the steep closing costs; and (4) the use of funds qualifies for the mortgage interest deduction under the Tax Cuts and Jobs Act (substantial home improvement, primarily).

If your existing mortgage is locked in at a sub-4% rate from 2020–2022, a cash-out refi today is rarely the right move — the rate increase on your full balance typically swamps any benefit from accessing equity. In that scenario, a HELOC or a sale (which eliminates the mortgage entirely) usually pencils better.

Option 3: Selling Your McLean Home

Selling is the only equity-access option that converts all of your equity into cash — not 80%, not what's left after a new mortgage. It's also the only option that ends your relationship with the asset entirely. For McLean homeowners contemplating downsizing, relocating, retirement repositioning, or simply cashing in on extraordinary appreciation, it's frequently the most powerful financial move available.

The Selling Timeline — Typical McLean Process

Listing Consultation & CMA — Week 1

Free in-home walkthrough, comparative market analysis, pricing strategy, and review of the 1.5% full-service program scope. No commitment required at this stage.

Pre-Listing Prep — Weeks 2–3

Touch-ups, decluttering, professional staging consult (often included), 4K photography, drone video, 3D Matterport tour. Most McLean homes need 1–3 weeks of light prep, not full renovations.

Active Listing — Weeks 4–7

MLS launch via BrightMLS, syndicated to Zillow/Realtor.com/Redfin, broker tour, weekend open houses, and private showings. McLean median days on market typically run 14–35 days for well-priced homes.

Offers & Negotiation — Variable

Multi-offer scenarios are common for McLean homes priced correctly. Strategy includes timing the offer-review window, escalation clauses, contingency negotiation, and (post-NAR settlement) explicit buyer-broker compensation negotiation.

Under Contract → Closing — 30–45 Days

Inspections, appraisal, financing contingency removal, title work, final walkthrough, and closing at a Northern Virginia title company. Sellers typically receive funds via wire same-day or next-day after closing.

McLean Sale Cost Breakdown — Where the Money Goes

| Cost | Traditional 3% | Jamil Brothers 1.5% |

|---|---|---|

| Listing agent commission (on $1.5M) | $45,000 | $22,500 |

| Buyer agent compensation (negotiable, often 2–2.5%) | $30,000–$37,500 | $30,000–$37,500 |

| Virginia grantor tax ($1 per $1,000) | $1,500 | $1,500 |

| NOVA regional congestion tax ($0.10 per $100) | $1,500 | $1,500 |

| Settlement/title/recording fees | $1,500–$3,000 | $1,500–$3,000 |

| HOA/condo transfer documents (where applicable) | $300–$700 | $300–$700 |

| Total seller costs (estimate) | ~$80,000+ | ~$58,000+ |

The single largest variable in your final net is the listing commission. Buyer-side compensation, transfer taxes, and settlement fees are roughly the same regardless of who lists your home. The listing fee is where the choice actually moves the needle — and on a $1.5M McLean home, that choice is worth $22,500 in your pocket at closing.

Run a personalized seller net sheet for your McLean home. Every cost broken down — listing commission, buyer-side compensation, Virginia transfer taxes, NOVA congestion tax, settlement fees, HOA transfers — so you know your real bottom line before you decide.

Side-by-Side Comparison: HELOC vs. Cash-Out Refi vs. Sale

| Factor | HELOC | Cash-Out Refi | Sale |

|---|---|---|---|

| Max equity accessed | ~80% LTV minus 1st mortgage | ~80% LTV minus 1st mortgage | 100% (after costs) |

| Upfront costs | $500–$1,500 | $15,000–$30,000 | $58K (1.5%) or $80K+ (3%) |

| Rate type | Variable (Prime + margin) | Fixed for life of loan | N/A — no debt |

| Time to funds | 2–4 weeks | 4–8 weeks | 8–12 weeks (list to close) |

| Affects current mortgage rate? | No — preserves existing rate | Yes — replaces with new rate | N/A — pays off entirely |

| Keep the home? | Yes | Yes | No |

| Tax-deductible interest? | Only if used for home improvement | Only on portion used for home improvement | Capital gains exclusion may apply |

| Best when… | You need flexibility and have a low first mortgage rate | Current rates ≤ existing rate, large lump sum needed | Downsizing, relocating, or maximizing equity capture |

Tax Implications of Each Option

Tax treatment is one of the most misunderstood aspects of equity access. The bottom line: borrowing against your home isn't taxable income (loan proceeds never are), but the deductibility of the interest you pay depends entirely on what you use the money for. Selling is the option with the most tax exposure — and ironically, also the option that often delivers the largest after-tax cash result for McLean homeowners.

HELOC and Cash-Out Refi Interest Deduction

Under the Tax Cuts and Jobs Act of 2017 (currently in effect through tax year 2025, with potential extensions), interest on home equity debt is deductible only if the proceeds are used to "buy, build, or substantially improve" the home that secures the loan. Using HELOC or cash-out refi funds to pay off credit cards, fund a wedding, buy an investment property, or pay tuition does not qualify — that interest is non-deductible. The total mortgage debt subject to deduction is also capped at $750,000 for loans originated after Dec. 15, 2017 ($1M for older loans grandfathered in).

Sale: The Capital Gains Exclusion

When you sell your primary residence, federal tax law lets you exclude up to $250,000 of capital gains if you're single, or $500,000 if you're married filing jointly — provided you've owned and lived in the home for at least 2 of the past 5 years. For long-tenured McLean homeowners, this is meaningful: if you bought in 2008 for $700K and sell in 2026 for $1.7M, your $1M gain is partially shielded ($500K MFJ exclusion), with the remaining $500K subject to long-term capital gains rates (typically 15–20% federal, plus the 3.8% net investment income tax for higher earners, plus Virginia's flat 5.75% state income tax).

⚠️ McLean Homes Often Exceed the Exclusion

If you've owned a McLean home since the early 2000s or earlier, your appreciation likely exceeds $500K — meaning a portion of your gain is taxable. Track every capital improvement (additions, kitchen/bath remodels, roof replacement, finished basement) — these adjust your cost basis upward and reduce taxable gain. A meeting with a CPA before listing is strongly recommended for high-equity sellers.

How to Choose the Right Option

The right answer depends on five questions. Run through each, and the path will usually become obvious.

ℹ️ The 5-Question Decision Framework

- Do you want to keep the home? If no — sale wins.

- What's your existing mortgage rate? If sub-4%, avoid cash-out refi unless current rates are similar.

- How much do you need, and how soon? Flexible draws over years → HELOC. Single large lump sum → refi or sale.

- How long will you stay? Cash-out refi closing costs only amortize sensibly with 5+ years of remaining ownership.

- What's the use of funds? Substantial home improvement preserves the interest deduction; non-improvement use doesn't.

Common McLean Scenarios

Match Your Situation to the Right Option

- Renovating a McLean kitchen ($150K project) with a 3% existing mortgage → HELOC

- Funding two college educations ($300K total) over 6 years → HELOC (flexibility) or partial cash-out refi

- Empty-nest downsize to a Vienna or Reston condo → Sale

- Retirement relocation to Florida or the Carolinas → Sale (capital gains exclusion + low-tax state)

- Paying off high-interest credit card debt ($80K) → HELOC (smaller, lower-fee transaction)

- Buying a vacation home in the Outer Banks → Cash-out refi or sale (if rebalancing portfolio)

If you need to access equity quickly — death in the family, divorce, job relocation, or estate situation — a cash offer can close in 14–21 days without inspections, financing contingencies, or showings. We'll walk you through the trade-off between speed and price, with no pressure.

McLean Market in 2026 — Impact on Each Option

Local market conditions change which equity strategy makes the most sense. Here's how the 2026 McLean environment shapes each path.

For HELOC and Cash-Out Refi Borrowers

McLean's continued price strength is a tailwind. Higher appraised values mean higher accessible equity at the same 80% LTV cap. The trade-off: federal interest rates have remained elevated relative to the 2020–2022 era, so the cost of borrowing — both on HELOCs (variable, indexed to Prime) and cash-out refis (fixed) — is higher than McLean homeowners with sub-4% mortgages remember. This is the central reason HELOCs have outpaced cash-out refis in popularity since 2023: they let you borrow at today's higher rates only on the new debt, while preserving your low first-mortgage rate.

For Sellers

McLean's seller environment in 2026 favors well-prepared, well-priced listings. Inventory remains relatively tight, particularly in the upper-tier $1.5M–$3M bracket. Days-on-market for properly staged and photographed homes typically run 14–35 days, with multi-offer scenarios still common in the spring and early-fall windows. The post-NAR settlement landscape (effective August 2024) has reshaped buyer-broker compensation: buyer agent commissions are now negotiated explicitly between buyer and their agent, and listing agreements no longer pre-commit the seller to paying buyer-side commission. In practice, McLean sellers are still typically offering 2–2.5% to buyer agents to attract buyer activity, but the structure is now transparent rather than embedded — and that transparency is one more reason listing-fee transparency (1.5% vs. 3%) deserves equal scrutiny.

The Hidden Cost of Selling: Why 1.5% Matters

If you decide that selling is the right path for accessing your equity, the single biggest variable you control is your listing commission. Use the calculator below to see exactly how much more you keep at 1.5% vs. a traditional 3% listing fee — at the price points most relevant to McLean.

Seller Savings Calculator

How much more do you keep with our 1.5% listing fee?

Select your home's estimated value to see your real net proceeds — side by side. (McLean homes typically fall in the $1M+ range.)

Traditional Agent — 3%

Our Fee — Only 1.5%

Extra in your pocket

$6,000

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

Our Fee — Only 1.5%

Extra in your pocket

$7,500

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

Our Fee — Only 1.5%

Extra in your pocket

$9,000

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

Our Fee — Only 1.5%

Extra in your pocket

$11,250

vs. a traditional 3% listing agent — with zero reduction in service or marketing.

Traditional Agent — 3%

Our Fee — Only 1.5%

Extra in your pocket

$15,000

vs. a traditional 3% listing agent — and the savings scale linearly. On a $1.5M McLean home, that's $22,500. On a $2M home, $30,000.

Estimates only. Actual closing costs vary. Buyer's agent commission is negotiable post-NAR settlement.

4K photography, drone video, 3D Matterport tours, expert pricing strategy, partner-led negotiation, and full BrightMLS marketing — all included at 1.5%. Same service as a 3% agent, with the difference deposited in your account at closing.

Common Equity Mistakes McLean Homeowners Make

Avoid These Six Costly Errors

- Refinancing out of a 3% mortgage just to access $200K of equity. The rate increase on the full balance often costs more than the equity is worth. A HELOC keeps the existing rate intact.

- Ignoring the capital gains exclusion when selling. If you've owned long enough to exceed the $250K/$500K thresholds, plan around it — sometimes a 6-month delay creates a major tax difference.

- Trusting Zestimate or Redfin Estimate for the equity calculation. Algorithmic valuations frequently misprice McLean homes by $100K+. Get a real CMA before sizing any HELOC or refi.

- Defaulting to 3% listing commission without negotiating or shopping. Post-NAR settlement, listing fees are explicitly negotiable. On a $1.5M McLean home, the difference between 3% and 1.5% is $22,500 — your money.

- Drawing a HELOC and treating it like income. HELOC funds aren't free money — they're debt secured by your home. Mismanaged, they create foreclosure risk in a downturn.

- Forgetting to track capital improvements. Receipts for renovations, additions, and major systems work increase your cost basis and reduce taxable gain on sale. Most McLean owners under-track this and overpay tax.

Frequently Asked Questions

How much equity do I have in my McLean home?

Your equity equals your home's current market value minus the balance owed on your mortgage and any other liens. For a typical McLean home owned for 10 years, equity often falls in the $800,000 to $1.4 million range. The most reliable way to determine your specific equity is a comparative market analysis (CMA) from a local agent — automated estimates from Zillow or Redfin frequently misprice McLean homes by $100,000 or more because they can't account for finish level, lot size, and the McLean HS vs. Langley HS school pyramid effect.

What's the difference between a HELOC and a cash-out refinance in Virginia?

A HELOC is a revolving credit line at a variable rate (Prime + a margin), with low closing costs ($500–$1,500), drawn flexibly over 10 years. A cash-out refinance replaces your existing mortgage with a new larger one at a fixed rate, delivering a single lump sum, with substantial closing costs ($15,000–$30,000 on a McLean-sized loan). HELOCs are best for flexible, shorter-term needs and preserve your existing first-mortgage rate; cash-out refis are best for large lump sums and long ownership horizons. The same Virginia regulations and federal tax rules apply to both.

How much does it cost to sell a $1.5M home in McLean?

Total seller costs on a $1.5M McLean home run roughly $58,000 with a 1.5% listing fee (Jamil Brothers full-service program) or $80,000+ with a traditional 3% listing fee. Both totals include buyer-agent compensation (negotiable, typically 2–2.5%), Virginia grantor tax ($1 per $1,000), the NOVA regional congestion tax ($0.10 per $100), settlement and title fees ($1,500–$3,000), and HOA transfer fees if applicable. The listing commission is the single largest controllable variable — you can run a personalized net sheet to see your specific numbers.

How long does each equity-access option take?

A HELOC typically funds in 2–4 weeks from application. A cash-out refinance takes 4–8 weeks due to full underwriting, appraisal, and title work. Selling a McLean home, from listing-consultation to cash in your bank account, typically runs 8–12 weeks (1–3 weeks of prep, 2–5 weeks active on the market, 30–45 days under contract through closing). A cash offer can close in as little as 14–21 days but typically delivers a lower price than an open-market sale.

Is HELOC interest tax-deductible in 2026?

Under the Tax Cuts and Jobs Act (currently in effect through tax year 2025, with possible extensions), HELOC and cash-out refi interest is deductible only if the proceeds are used to "buy, build, or substantially improve" the home that secures the loan. Using the funds for credit card payoff, tuition, or non-home purposes makes the interest non-deductible. Total mortgage debt subject to deduction is capped at $750,000 for loans originated after December 15, 2017. Always consult a CPA for your specific situation.

Should I sell my McLean home or take out a HELOC?

Sell if you want to stop owning the home, capture 100% of your equity, exit a property that no longer fits your stage of life, or relocate. HELOC if you want to keep the home, need flexible access to a portion of your equity, and have a low first-mortgage rate worth preserving. Selling unlocks more cash overall but costs more upfront and ends ownership; a HELOC borrows against your equity at modest cost but leaves you with new debt to repay. Many McLean owners run both scenarios on a personalized net sheet before deciding.

What is the post-NAR settlement, and how does it affect a McLean sale?

Effective August 17, 2024, the National Association of Realtors settlement changed how buyer-agent compensation is structured. Listing agreements no longer pre-commit sellers to paying buyer-side commission, and buyer-broker compensation is now negotiated explicitly between buyers and their agents (and confirmed in a buyer-broker agreement before tours begin). In practice, McLean sellers still typically offer 2–2.5% to attract buyer activity, but the structure is transparent rather than embedded in a single commission number. The settlement also reinforced that listing-side commissions are fully negotiable — making the 1.5% vs. 3% choice a clear, conscious decision for sellers rather than a default.

How do I choose a listing agent for a McLean sale?

Evaluate four objective criteria: (1) recent McLean transaction volume — agents with 5+ McLean closings in the past 12 months understand the local pricing nuances; (2) marketing scope — professional 4K photography, drone video, and 3D tours should be included, not upsold; (3) commission transparency — what's included, and is the listing fee negotiable; (4) recent reviews — Google, Zillow, and Realtor.com reviews from the last 12 months. The Jamil Brothers Realty Group meets these criteria with 840+ closings, $500M+ volume, NVAR Lifetime Top Producer status, 500+ five-star reviews, and a 1.5% full-service listing fee that includes all marketing components.

What HOA considerations exist for selling in McLean?

Most McLean detached homes are not in HOAs, but several established neighborhoods (Hallcrest, McLean Hamlet, Pimmit Hills sections, Tysons-area condos and townhomes) do have HOA or condo association requirements. Sellers in HOA communities must order a "resale package" or "condo questionnaire" — typically $300–$700 — which discloses dues, special assessments, reserve studies, and bylaws to the buyer. Order this 30–45 days before listing to avoid closing delays. Virginia law (POA Act and Condo Act) gives buyers a 3-day right of cancellation after receiving the package.

Can I do a HELOC and then sell within a year?

Yes. The HELOC will be paid off at closing as part of the title settlement — same as your first mortgage. Some HELOCs have an "early closure fee" if you terminate within the first 2–3 years (typically $300–$500), but this is a small expense relative to the proceeds of a McLean sale. Confirm your HELOC's early-closure terms before drawing if you anticipate selling soon. Selling fully resolves the HELOC; you keep whatever equity remains after paying off both the first mortgage and the HELOC, plus closing costs.

How does the capital gains exclusion work for a McLean home sale?

If you've owned and lived in your McLean home as your primary residence for at least 2 of the past 5 years, you can exclude up to $250,000 of capital gain (single filer) or $500,000 (married filing jointly) from federal taxation. Gain above the exclusion is subject to long-term capital gains rates — typically 15% or 20% federal, plus the 3.8% Net Investment Income Tax for higher earners, plus Virginia's 5.75% state income tax. Long-tenured McLean owners frequently exceed the exclusion. Track every capital improvement (roof, HVAC, kitchen/bath remodels, additions) — these increase your cost basis and reduce taxable gain. A CPA consultation before listing is strongly recommended for any sale expected to exceed the exclusion.

What's the average days on market for a McLean home in 2026?

Days on market in McLean (22101 and 22102) for properly priced and presented homes typically run 14–35 days in 2026, with multi-offer scenarios still common during the spring (March–May) and early-fall (September) windows. Mispriced homes — typically those listed 5%+ above CMA-supported values — extend significantly, often hitting 60–90 days with one or more price reductions. Inventory in the upper-tier $1.5M–$3M bracket remains relatively tight, supporting strong pricing for well-prepared listings. Days-on-market data from BrightMLS is the gold standard reference for these figures.

Glossary

Equity

Your home's market value minus what you owe on it. The portion of the home you actually own outright.

HELOC

Home Equity Line of Credit. A revolving credit line secured by your home, typically with a variable rate.

Cash-Out Refinance

A new, larger mortgage that replaces your existing one — you receive the difference as cash at closing.

LTV (Loan-to-Value)

The ratio of your loan balance to your home's appraised value. Most home equity lending caps at 80% combined LTV.

CMA

Comparative Market Analysis. A local agent's pricing study based on recent comparable sales in your specific neighborhood.

Grantor Tax

Virginia's seller-paid transfer tax: $1 per $1,000 of sale price, paid at closing.

NOVA Congestion Tax

Northern Virginia's regional transportation tax: $0.10 per $100 of sale price for properties in qualifying NOVA jurisdictions.

Capital Gains Exclusion

Federal tax provision allowing up to $250K (single) or $500K (MFJ) of profit on a primary-residence sale to be excluded from tax.

Explore More McLean & Northern Virginia Guides

Conclusion: Make the Decision That Fits Your Life

There is no universal "best" way to access your McLean home equity — there's only the option that fits your situation: your existing mortgage rate, your timeline, your tax position, your long-term plan, and whether the home itself still fits the next chapter of your life. A HELOC offers low-friction flexibility. A cash-out refinance delivers a fixed-rate lump sum. A sale converts every dollar of equity into liquid capital you can deploy anywhere.

What's universal is that the decision deserves real numbers behind it — not algorithmic estimates, not internet rules of thumb, and certainly not a default 3% commission accepted out of habit. The Jamil Brothers Realty Group provides street-level home valuations, personalized seller net sheets, and the full 1.5% full-service listing program for sellers who decide that a sale is the right path. There's no cost, no obligation, and no pressure — just clear information and clear math, so you can make the choice with confidence.

Know your real equity. Compare your three options with actual numbers — not estimates. The Jamil Brothers provide a full seller consultation at no cost, walking you through HELOC, cash-out refi, and sale scenarios specific to your McLean home. Response within 24 hours. Decisions of this size deserve real data.

The Jamil Brothers Realty Group · Saad Jamil & Arslan Jamil · Samson Properties · NVAR Lifetime Top Producers · Licensed in VA, MD, DC, and WV · (703) 782-4830

Explore More

Browse Every Corner of the DMV Market

Whether you're searching by budget, neighborhood, or buying situation — find exactly what you need below.

Virginia Homes by Budget

Washington DC Homes by Budget

Maryland Homes

Explore Northern Virginia Communities

Loudoun County

Fairfax County & Surrounding

Ready to Make a Move?

Full-Service · No Tradeoffs

List for 1.5% & Keep More Equity

Professional photography, drone video, 3D tours, and expert negotiation — all included. On an $800K home, that's $12,000 more in your pocket vs. a 3% agent.

See the 1.5% Program →Need Speed or Certainty?

Get a No-Obligation Cash Offer

Skip the showings, skip the contingencies. If timing or condition matters more than top dollar, a cash offer may be the right fit. We'll walk you through every option.

Explore Cash Offers →Categories

Recent Posts

Let's Connect